Offshore Grantor Trusts: The Gift Election That Backfires

Offshore asset protection trusts — particularly those established in jurisdictions like the Cook Islands, Nevis, and the Cayman Islands — remain among the most powerful tools available to U.S. clients seeking to shield wealth from future creditors.

At Dilendorf Law Firm, we regularly assist clients in structuring, analyzing, and maintaining foreign grantor trusts that are legally sound, tax compliant, and built to withstand scrutiny.

But “built to withstand scrutiny” is the operative phrase.

The gift tax election is one of the most consequential decisions in offshore trust planning — and one of the most misunderstood.

At its core, it comes down to a single question: when you transfer assets to the trust, does the IRS treat that transfer as a completed gift or an incomplete one?

This election carries deep implications not just for estate and gift taxes, but for how the trust performs if it is ever challenged by a creditor in litigation.

The Completed vs. Incomplete Gift Election

A completed gift occurs when the settlor permanently gives up all rights, authority, and control over the transferred property.

Although the transfer may incur gift tax or reduce the settlor’s available lifetime exemption, the assets are excluded from the settlor’s taxable estate.

In addition, any future increase in the assets’ value passes free of estate tax, creating a significant advantage for clients transferring assets expected to appreciate substantially.

An incomplete gift, by contrast, occurs when the settlor retains certain powers over the trust — such as a testamentary or lifetime power of appointment, the ability to change beneficiaries, or a power exercisable in conjunction with an adverse party.

Because the settlor has not fully relinquished control, no gift tax is triggered. The assets remain in the settlor’s taxable estate, but no exemption is consumed at funding.

From a purely tax-efficiency standpoint, the incomplete gift election is attractive.

The client transfers assets, achieves creditor protection under foreign law, pays no gift tax, and continues to report trust income on their personal return as a grantor trust under IRC §§ 671–679.

It appears to be the best of all worlds.

It is not.

The Dangerous Contradiction Built Into the Incomplete Gift Structure

Here is where sophisticated clients — and their advisors — must be clear-eyed.

The retained powers that make the transfer an incomplete gift for tax purposes do not disappear in litigation.

A creditor’s attorney will use those exact same powers to argue that the trust is the debtor’s alter ego, that the assets are reachable, and that the entire structure should be collapsed.

The incomplete gift election creates a structural contradiction. The client is effectively taking two mutually inconsistent positions:

- For asset protection purposes: “I have no control over these assets. They belong to an independent foreign trust, administered by a foreign trustee, under foreign law. You cannot reach them.”

- For federal tax purposes: “These assets are mine. I report all trust income on my personal tax return. I retain powers over this trust. I am the grantor-owner under the Internal Revenue Code.

In litigation, a creditor’s attorney will exploit this contradiction with precision.

How a Creditor Attacks: Discovery, Depositions, and the Courtroom Argument

- Federal tax returns (Form 1040) — showing the debtor reported grantor trust income year after year, treating the trust assets as their own for income tax purposes

- Form 3520 and Form 3520-A — the annual reporting forms the IRS requires of U.S. persons who own or transfer property to foreign trusts; these forms contain explicit representations of ownership and control

- FBAR filings (FinCEN 114) — confirming the debtor’s ongoing financial interest in the foreign account

- Trust documents — the trust deed, any letters of wishes, and correspondence with the foreign trustee that reveal the retained powers relied upon for incomplete gift status.

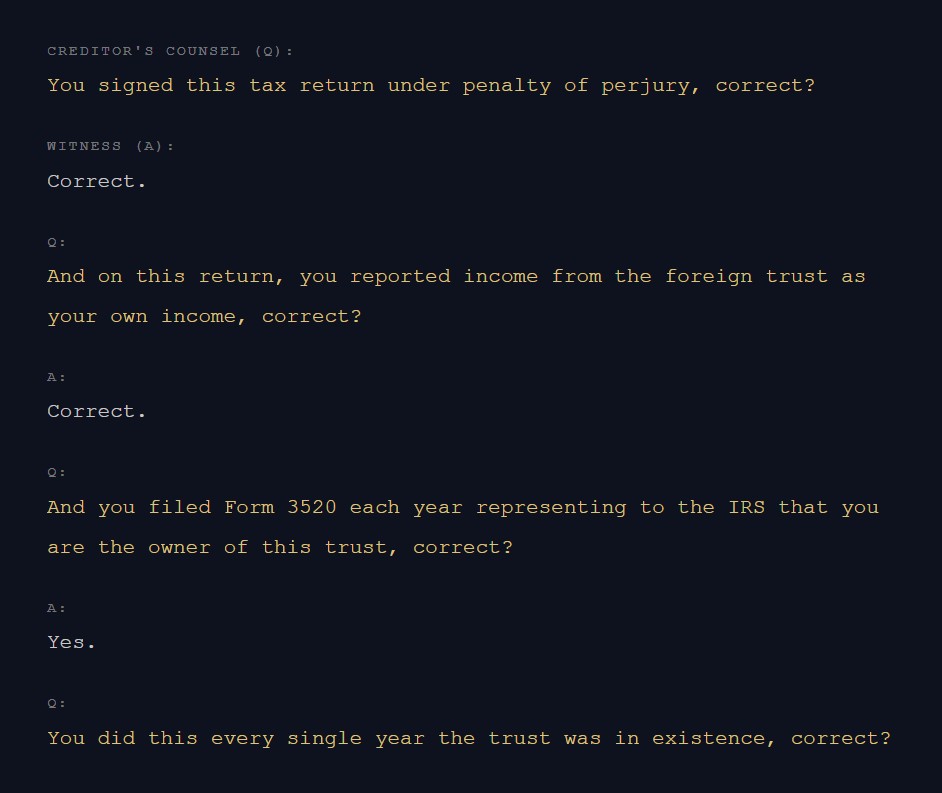

In deposition, the debtor will be walked through each filing, year by year. The questioning is methodical:

“You signed this tax return under penalty of perjury, correct? And on this return, you reported income from the foreign trust as your own income, correct? And you filed Form 3520 representing to the IRS that you are the owner of this trust, correct? You did this every year the trust was in existence, correct?”

Then, before the judge, creditor’s counsel makes the argument in plain terms:

“Your Honor, the debtor cannot have it both ways. For fifteen years, he told the federal government — under penalty of perjury — that he owned these assets. He claimed the grantor trust tax treatment. He reported the capital gains, the dividends, the interest. He used the incomplete gift election specifically to avoid paying gift tax on the transfer, taking the position that he never truly gave these assets away. Now, standing before this Court with a judgment against him, he claims he has no control over, and no access to, these same assets. He has built his entire tax strategy on the proposition that these assets are his — and we ask this Court to hold him to that position.”

What Clients Must Understand Before They Structure

This does not mean offshore trusts are ineffective or that the incomplete gift election is always wrong.

It means that every planning decision carries trade-offs that must be understood before the trust is funded, not after a judgment is entered.

Clients who prioritize maximum asset protection credibility should seriously consider the completed gift election — accepting the gift tax cost or exemption consumption in exchange for a legally consistent position: the assets were transferred, the gift was made, and the debtor retains no powers that would support a claim of ownership.

Clients who elect incomplete gift treatment for tax reasons must understand that they are accepting a structural vulnerability — one that a skilled creditor’s attorney will find in the first round of document requests.

At Dilendorf Law Firm, our approach to foreign trust planning begins with this conversation. We analyze the client’s exposure profile, the likely creditor universe, the tax cost of each election, and the long-term litigation posture of the structure.

The most tax-efficient trust is not always the most defensible one. Getting that balance right — before the trust is funded and before litigation begins — is exactly the kind of analysis our clients rely on us to provide.

Dilendorf Law Firm advises U.S. and international clients on offshore trust structuring, foreign grantor trust tax compliance, international estate planning, and asset protection strategies.

For a consultation, contact our office at dilendorf.com.

This article is for informational purposes only and does not constitute legal or tax advice. Readers should consult qualified legal counsel before making any planning decisions.

Resources

IRS Forms & Reporting Requirements

- About Form 3520 — Annual Return to Report Transactions With Foreign Trusts — IRS official page for Form 3520, filed by U.S. persons who own or transfer assets to a foreign trust

- About Form 3520-A — Annual Information Return of Foreign Trust With a U.S. Owner — Required annual filing by the foreign trust itself; a critical source of ownership admissions in discovery

- Foreign Trust Reporting Requirements and Tax Consequences — IRS overview of all reporting obligations for U.S. owners and beneficiaries of foreign trusts

- Report of Foreign Bank and Financial Accounts (FBAR) — FinCEN Form 114 filing obligations for U.S. persons with foreign financial interests

Internal Revenue Code & Treasury Regulations

- Treas. Reg. § 25.2511-2 — Cessation of Donor’s Dominion and Control — The governing regulation defining complete vs. incomplete gifts; the foundation of the incomplete gift election

- IRC § 2511 — Transfers in General — Statutory basis for the gift tax and the transfer analysis

- IRC § 2501 — Imposition of Gift Tax — The completed gift tax imposition provision

- IRC § 679 — Foreign Trusts Having One or More U.S. Beneficiaries — Grantor trust treatment for foreign trusts; the provision that makes the settlor the tax owner

- IRC §§ 671–679 — Grantor Trust Rules (Full Subpart E) — Complete grantor trust rule framework governing income tax treatment

Case Law

- FTC v. Affordable Media, LLC, 179 F.3d 1228 (9th Cir. 1999) — The landmark Cook Islands trust contempt case; established that self-induced impossibility is not a defense to a repatriation order

Cook Islands Legal Framework

- Cook Islands International Trusts Act 1984 — Overview — Summary of the Act’s key asset protection provisions including the foreign judgment bar and fraudulent disposition limitations

- Cook Islands Financial Services Development Authority — International Trusts Fact Sheet — Official government fact sheet on the Cook Islands trust structure

- Cook Islands ITA Section 13B — Fraudulent Conveyance Explained — Official explanation of the 2-year limitation period for creditor challenges under Cook Islands law