Family limited partnerships (“FLPs”) are often used in estate planning and asset protection. When properly structured, an FLP can centralize family asset management, restrict transfers, separate management rights from economic rights, and make it harder for a creditor of one partner to reach specific partnership property.

But FLPs are not perfect asset protection structures. Courts may respect the partnership form and still allow a creditor to reach the debtor-partner’s economic interest.

In some cases, a charging order can lead to foreclosure or sale of the partnership interest itself.

The key distinction is between partnership property and the partner’s interest in the partnership. A creditor may be blocked from directly seizing partnership assets, but the debtor-partner’s economic rights may still be vulnerable.

A Creditor Usually Cannot Seize Partnership Assets Directly

The starting point is that a judgment against an individual partner is not the same as a judgment against the partnership.

In Crocker National Bank v. Perroton, 208 Cal. App. 3d 1, 255 Cal. Rptr. 794 (Cal. Ct. App. 1989), the California Court of Appeal explained:

“A creditor with a judgment against a partner but not against the partnership ordinarily cannot execute directly on partnership assets or on the partner’s interest in the partnership.”

That rule is important for FLP planning. It means that a personal creditor of one partner generally cannot simply levy on partnership real estate, investment accounts, or other assets merely because that partner owes a personal debt.

The court also explained why the charging order remedy exists. It was designed to prevent disruption of the partnership business and protect the interests of the other partners:

“It was to prevent such ‘hold up’ of the partnership business and the consequent injustice done the other partners resulting from execution against partnership property that the quoted code sections and their counterparts in the Uniform Partnership Act and the English Partnership Act of 1890 were adopted.”

This is one reason FLPs can provide meaningful protection: the charging-order remedy is designed to prevent a personal creditor of one partner from disrupting the partnership business or executing directly against partnership property.

However, that protection is not absolute; the creditor may still reach the debtor-partner’s economic interest through a charging order and, in some circumstances, seek sale or foreclosure of that interest.

The Creditor’s Remedy Is Usually a Charging Order

Because the law generally protects partnership property from direct execution for the personal debt of one partner, a creditor usually must proceed in a more limited way. Instead of seizing partnership assets, the creditor typically seeks a charging order against the debtor-partner’s partnership interest.

“Therefore, a judgment creditor must seek a charging order to reach the debtor partner’s interest in the partnership.”

A charging order does not usually give the creditor control over the partnership or direct ownership of partnership property. Instead, it allows the court to charge the debtor-partner’s economic interest with payment of the unsatisfied judgment.

The court then described what a charging order can do:

“Through a charging order, the court may charge the debtor’s interest in the partnership with payment of the unsatisfied judgment, plus interest. The court may also appoint a receiver of subsequent profits or other money due to the debtor partner.”

In practical terms, the charging order does not necessarily give the creditor control over the FLP. But it may redirect distributions that would otherwise go to the debtor-partner.

“The charging order leaves the partnership intact but diverts to the judgment creditor the debtor partner’s share of the profits.”

The court also emphasized the limits of a charging creditor’s rights:

“It is important to note that a charging creditor does not become a full partner, is not entitled to manage the partnership, and has no right to attach specific partnership property.”

This distinction is critical. A charging creditor may not step into the shoes of a full partner. The creditor may not automatically receive management rights. But the creditor may still reach economic rights attached to the debtor-partner’s interest.

A Charging Order Can Lead to Sale of the Partnership Interest

The major risk is that a charging order may not be the end of the enforcement process.

In Crocker, the creditor obtained a judgment against Jon Perroton and then obtained a charging order against his limited partnership interest. When the charging order did not result in payment, the creditor moved for sale of Perroton’s interest in the partnership.

The court noted:

“As of November 1985, Crocker had received no monies as a result of the charging order against Turn-Key Storage. Therefore, on November 26, 1985, Crocker moved for an order of sale of Perroton’s interest in Turn-Key Storage.”

The court ultimately allowed the sale of the debtor-partner’s interest, while distinguishing that interest from the partnership’s own property:

“We conclude that the authorities support the order for sale of a judgment debtor partner’s partnership interest as distinct from the property of the limited partnership, where the creditor has shown that it was unable to obtain satisfaction of the debt under the charging order, and where the remaining partner, here the general partner Bette Perroton, has consented to the sale.”

This is a key lesson for FLP planning. The partnership assets may be protected from direct execution, but the debtor-partner’s interest may still be charged and sold if the facts and governing law support that remedy.

The Purchaser Does Not Necessarily Receive Full Partner Rights

The sale of a partnership interest does not necessarily mean that the purchaser becomes a full partner or gains control over the partnership. In Crocker, the court explained:

“Just as a charging order cannot grant the creditor a greater interest in the partnership than that of the debtor partner at the time of the order . . . a supplementary order for sale, does not allow the purchaser to acquire more rights in the partnership than the debtor partner possessed.”

The court also noted:

“Further, both the limited partnership agreement and the consent to the sale by Bette Perroton make clear that a purchaser of Perroton’s limited partnership interest would have rights to profits and losses, but would not become a substituted limited partner in the partnership, absent consent by the general partner.”

This is where careful drafting matters. A well-drafted FLP agreement may limit what a creditor or purchaser receives, but it may not prevent the creditor from reaching the debtor-partner’s transferable economic interest.

Foreclosure of the Partnership Interest

Madison Hills shows another important risk: foreclosure. There, the creditor sought a charging order and strict foreclosure of the debtor’s partnership interest. The trial court ordered that “the partnership interest be foreclosed unless redeemed by the defendant prior to April 15, 1993.”

On appeal, the Connecticut Appellate Court confirmed that foreclosure was available:

“Foreclosure is one of the orders available to charging creditors.”

The court further concluded:

“We conclude, therefore, that the UPA does permit a charging creditor to enforce its charging order through strict foreclosure.”

For FLP planning, this is significant. A charging order may begin as a remedy limited to distributions, but in some jurisdictions and under some circumstances, it may lead to foreclosure of the debtor-partner’s interest.

Conclusion

Family limited partnerships can be useful estate planning and asset protection tools, but they are not creditor-proof.

Courts may protect partnership assets from direct seizure while still allowing a creditor to reach the debtor-partner’s economic interest through a charging order, sale, or foreclosure.

The key is careful planning. FLPs should be properly structured, funded, and documented before creditor issues arise. A well-drafted partnership agreement can limit what a creditor or purchaser receives, but it cannot eliminate all enforcement risk.

Contact Us

At Dilendorf Law Firm, we provide tailored legal solutions for high-net-worth individuals and families seeking to preserve wealth, maintain control, and plan for future generations.

We help U.S. and non-U.S. clients with estate planning, asset protection, family limited partnerships, domestic and international trust structures, and creditor-risk analysis.

If you’re considering a Family Limited Partnership as part of your estate or asset protection strategy, our team is here to help. Contact us at (212) 457-9797 or email us at info@dilendorf.com.

Offshore asset protection trusts — particularly those established in jurisdictions like the Cook Islands, Nevis, and the Cayman Islands — remain among the most powerful tools available to U.S. clients seeking to shield wealth from future creditors.

At Dilendorf Law Firm, we regularly assist clients in structuring, analyzing, and maintaining foreign grantor trusts that are legally sound, tax compliant, and built to withstand scrutiny.

But “built to withstand scrutiny” is the operative phrase.

The gift tax election is one of the most consequential decisions in offshore trust planning — and one of the most misunderstood.

At its core, it comes down to a single question: when you transfer assets to the trust, does the IRS treat that transfer as a completed gift or an incomplete one?

This election carries deep implications not just for estate and gift taxes, but for how the trust performs if it is ever challenged by a creditor in litigation.

The Completed vs. Incomplete Gift Election

When a U.S. person transfers assets to a foreign grantor trust, the transfer is analyzed under IRC § 2511 and Treasury Regulation § 25.2511-2 to determine whether a taxable gift has occurred.

A completed gift occurs when the settlor permanently gives up all rights, authority, and control over the transferred property.

Although the transfer may incur gift tax or reduce the settlor’s available lifetime exemption, the assets are excluded from the settlor’s taxable estate.

In addition, any future increase in the assets’ value passes free of estate tax, creating a significant advantage for clients transferring assets expected to appreciate substantially.

An incomplete gift, by contrast, occurs when the settlor retains certain powers over the trust — such as a testamentary or lifetime power of appointment, the ability to change beneficiaries, or a power exercisable in conjunction with an adverse party.

Because the settlor has not fully relinquished control, no gift tax is triggered. The assets remain in the settlor’s taxable estate, but no exemption is consumed at funding.

From a purely tax-efficiency standpoint, the incomplete gift election is attractive.

The client transfers assets, achieves creditor protection under foreign law, pays no gift tax, and continues to report trust income on their personal return as a grantor trust under IRC §§ 671–679.

It appears to be the best of all worlds.

It is not.

The Dangerous Contradiction Built Into the Incomplete Gift Structure

Here is where sophisticated clients — and their advisors — must be clear-eyed.

The retained powers that make the transfer an incomplete gift for tax purposes do not disappear in litigation.

A creditor’s attorney will use those exact same powers to argue that the trust is the debtor’s alter ego, that the assets are reachable, and that the entire structure should be collapsed.

The incomplete gift election creates a structural contradiction. The client is effectively taking two mutually inconsistent positions:

For asset protection purposes: “I have no control over these assets. They belong to an independent foreign trust, administered by a foreign trustee, under foreign law. You cannot reach them.”

For federal tax purposes: “These assets are mine. I report all trust income on my personal tax return. I retain powers over this trust. I am the grantor-owner under the Internal Revenue Code.

In litigation, a creditor’s attorney will exploit this contradiction with precision.

How a Creditor Attacks: Discovery, Depositions, and the Courtroom Argument

The attack begins in discovery. Creditor’s counsel will serve document production requests targeting:

Federal tax returns (Form 1040) — showing the debtor reported grantor trust income year after year, treating the trust assets as their own for income tax purposes

Form 3520 and Form 3520-A — the annual reporting forms the IRS requires of U.S. persons who own or transfer property to foreign trusts; these forms contain explicit representations of ownership and control

FBAR filings (FinCEN 114) — confirming the debtor’s ongoing financial interest in the foreign account

Trust documents — the trust deed, any letters of wishes, and correspondence with the foreign trustee that reveal the retained powers relied upon for incomplete gift status.

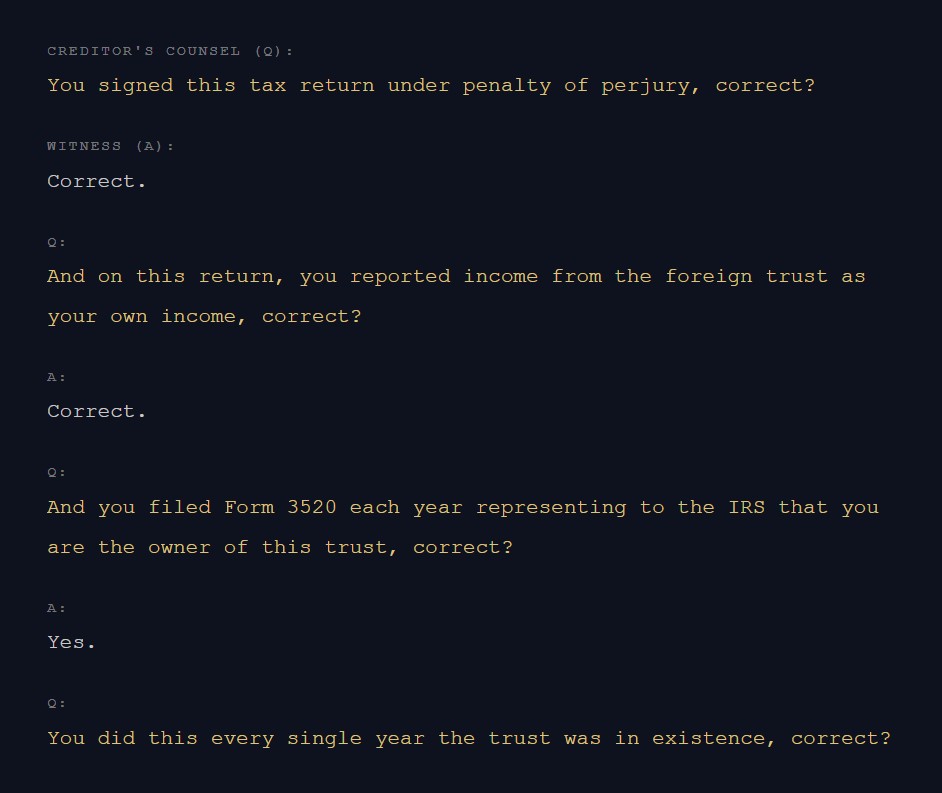

In deposition, the debtor will be walked through each filing, year by year. The questioning is methodical:

“You signed this tax return under penalty of perjury, correct? And on this return, you reported income from the foreign trust as your own income, correct? And you filed Form 3520 representing to the IRS that you are the owner of this trust, correct? You did this every year the trust was in existence, correct?”

Then, before the judge, creditor’s counsel makes the argument in plain terms:

“Your Honor, the debtor cannot have it both ways. For fifteen years, he told the federal government — under penalty of perjury — that he owned these assets. He claimed the grantor trust tax treatment. He reported the capital gains, the dividends, the interest. He used the incomplete gift election specifically to avoid paying gift tax on the transfer, taking the position that he never truly gave these assets away. Now, standing before this Court with a judgment against him, he claims he has no control over, and no access to, these same assets. He has built his entire tax strategy on the proposition that these assets are his — and we ask this Court to hold him to that position.”

This is the doctrine of judicial estoppel applied with full force. Courts cannot permit a party to assert one position to gain a tax benefit and then assert an incompatible position to escape a legal obligation.

What Clients Must Understand Before They Structure

This does not mean offshore trusts are ineffective or that the incomplete gift election is always wrong.

It means that every planning decision carries trade-offs that must be understood before the trust is funded, not after a judgment is entered.

Clients who prioritize maximum asset protection credibility should seriously consider the completed gift election — accepting the gift tax cost or exemption consumption in exchange for a legally consistent position: the assets were transferred, the gift was made, and the debtor retains no powers that would support a claim of ownership.

Clients who elect incomplete gift treatment for tax reasons must understand that they are accepting a structural vulnerability — one that a skilled creditor’s attorney will find in the first round of document requests.

At Dilendorf Law Firm, our approach to foreign trust planning begins with this conversation. We analyze the client’s exposure profile, the likely creditor universe, the tax cost of each election, and the long-term litigation posture of the structure.

The most tax-efficient trust is not always the most defensible one. Getting that balance right — before the trust is funded and before litigation begins — is exactly the kind of analysis our clients rely on us to provide.

Dilendorf Law Firm advises U.S. and international clients on offshore trust structuring, foreign grantor trust tax compliance, international estate planning, and asset protection strategies.

For a consultation, contact our office at dilendorf.com.

This article is for informational purposes only and does not constitute legal or tax advice. Readers should consult qualified legal counsel before making any planning decisions.

Many U.S. citizens and Green Card holders living abroad believe that once they move overseas and start paying taxes locally, their U.S. reporting obligations largely disappear.

In practice, that is often not the case.

The United States continues to impose extensive reporting requirements – even where no additional U.S. tax is due.

For many expats, the problem is not intentional noncompliance. The issue is that the rules are far more technical than people expect.

FBAR Reporting: Simple Rule, Complicated Reality

One of the most common reporting obligations is the FBAR, FinCEN Form 114, officially called the Report of Foreign Bank and Financial Accounts.

In general, a U.S. individual is required to submit an FBAR when the combined balance of their foreign financial accounts goes over $10,000 at any time during the year.

A U.S. person with either a financial interest in, or signature authority over, one or more foreign financial accounts is generally required to file an FBAR if the total value of those accounts exceeds $10,000 at any time during the calendar year.

What Constitutes a “Financial Interest”?

Many individuals incorrectly assume that only accounts held directly in their own name are reportable.

In reality, the definition of “financial interest” is substantially broader. A U.S. person may be treated as having a reportable financial interest where:

the individual is the owner of record or holds legal title to the account;

the account is maintained for the benefit of another person;

the account is held through certain foreign entities; or

the individual directly or indirectly owns more than 50% of the voting power, equity interest, assets, or profits of an entity holding the account.

As a result, FBAR reporting obligations may extend to foreign companies, family structures, trusts, or jointly managed assets.

In practice, many expats operate through structures that were perfectly ordinary in their home country but create unexpected U.S. reporting issues after immigration or acquisition of U.S. tax residency.

Signature Authority Can Trigger Filing Obligations

Another area that creates confusion is “signature authority.”

A person may have an FBAR filing obligation even if the money does not belong to them personally.

Under the rules, signature authority generally means the ability to control the movement of funds in a foreign account through direct communication with the financial institution.

This issue frequently appears in family businesses and international companies where an individual has authority to move funds operationally, even though they are not the beneficial owner of the account.

A surprisingly large number of expats discover FBAR exposure through accounts they viewed as merely administrative or business-related.

Joint Accounts and Family Accounts

FBAR reporting becomes particularly complicated in the context of jointly owned accounts and family relationships.

For example, some individuals are added to foreign accounts simply to help aging parents or relatives manage finances abroad.

Others maintain joint accounts with spouses or family members in their country of origin for practical reasons.

In some situations, spouses may rely on a single FBAR filing. In other cases, separate filings may still be necessary.

Children can also have independent FBAR obligations. Where a child cannot file, the parent or guardian may need to file on the child’s behalf.

These are not unusual situations and commonly arise in international families maintaining accounts outside the United States for estate planning, retirement, or ordinary family financial management.

Currency Conversion and Valuation Issues

Even determining whether the $10,000 threshold has been exceeded may require careful analysis.

Where accounts are denominated in foreign currency, FBAR rules require conversion into U.S. dollars using the applicable Treasury exchange rate for the last day of the calendar year. In certain situations, alternative verifiable exchange rates may be necessary.

This analysis becomes particularly important where:

multiple foreign currencies are involved;

cryptocurrency-related accounts are maintained abroad;

accounts fluctuate significantly during the year; or

foreign institutions use multiple exchange-rate systems.

FBAR Compliance Often Appears Simpler Than It Is

Many individuals assume that FBAR reporting is a relatively straightforward disclosure obligation.

In reality, the rules involve technical ownership concepts, attribution principles, and reporting requirements that may create significant exposure even where violations were entirely unintentional.

For many U.S. expats, compliance issues are identified only years later — frequently during expatriation planning, immigration review, foreign trust restructuring, or broader cross-border tax analysis.

The matters discussed above represent only a small sample of the issues that may arise in connection with FBAR reporting. Before making corrective submissions or providing expatriation-related certifications, it is generally prudent to conduct a thorough review of foreign accounts, ownership arrangements, signature authority, and prior filing history.

FATCA Reporting: A Separate Obligation

Many U.S. expats are familiar with the FBAR but are less aware of FATCA reporting requirements.

In practice, individuals are often surprised to learn that filing an FBAR does not necessarily satisfy their FATCA obligations.

FATCA, the Foreign Account Tax Compliance Act, generally requires certain U.S. taxpayers to report specified foreign financial assets on IRS Form 8938, which is filed together with the individual’s U.S. tax return.

Unlike the FBAR, which is filed with the U.S. Department of the Treasury through FinCEN, Form 8938 is submitted directly to the IRS as part of a taxpayer’s federal income tax filing.

The overlap between the two reporting systems creates confusion because some foreign assets may need to be reported on both forms, while others may appear only on one.

In practice, many expats do not realize there is a FATCA issue until years later, often during broader tax planning, expatriation planning, or immigration-related review.

FATCA Reporting Thresholds Are Different

FBAR filing obligations generally arise when the combined value of foreign financial accounts exceeds $10,000 at any time during the calendar year. In contrast, FATCA reporting thresholds are substantially higher and vary based on:

filing status, including marital status;

whether the taxpayer resides inside or outside the United States; and

the value and type of specified foreign financial assets.

For instance, U.S. taxpayers residing outside the United States are often subject to considerably higher FATCA reporting thresholds than those living domestically.

In certain situations, an unmarried individual living abroad may not have a FATCA filing obligation unless the value of specified foreign financial assets exceeds $200,000 at the end of the tax year or $300,000 at any point during the year.

As a result, some individuals may have an FBAR filing obligation but no FATCA filing requirement, while others may be required to file both forms.

FATCA Extends Beyond Traditional Bank Accounts

Many individuals associate FATCA exclusively with foreign bank accounts. In reality, FATCA reporting may apply to a much broader category of foreign financial assets.

foreign-issued life insurance or annuity products;

foreign pension arrangements;

foreign mutual funds;

and other specified foreign financial assets.

In some situations, assets may be reportable under FATCA but not under FBAR.

For example, foreign partnership interests or foreign stock held outside a financial account may trigger FATCA reporting even where no FBAR filing obligation exists.

At the same time, signature authority over a foreign financial account may create an FBAR filing obligation even where the account itself is not reportable under FATCA.

Determining whether a particular asset must be reported often requires careful review of ownership structure, valuation, and the taxpayer’s relationship to the asset.

FATCA Issues Are Often Discovered Years Later

For many U.S. expats, FATCA issues do not become apparent until years later — often during expatriation planning, immigration review, offshore restructuring, or preparation of amended tax filings.

In some cases, individuals first learn about FATCA after receiving requests from foreign financial institutions asking them to certify U.S. tax status or provide IRS forms such as Form W-9.

Foreign banks and financial institutions increasingly exchange information with U.S. authorities under FATCA-related reporting frameworks.

As a result, foreign account and asset reporting issues that previously remained unnoticed are now more likely to surface during routine compliance reviews.

The issues discussed above represent only a few examples of the complexities that may arise in FATCA compliance.

Before submitting amended filings, corrective disclosures, or expatriation-related certifications, careful review of foreign assets, reporting history, and ownership structures is often advisable.

Contact Us

Dilendorf Law Firm advises U.S. and international clients on FATCA and FBAR compliance, offshore reporting obligations, expatriation planning, and broader cross-border tax matters.

Our practice includes review of foreign account reporting issues involving FinCEN Form 114 (FBAR), IRS Form 8938 (FATCA), foreign trusts, offshore entities, and other international reporting requirements that may arise in connection with foreign financial assets and overseas structures.

We assist clients with compliance review, corrective filings, amended international reporting, and strategic planning involving foreign accounts, ownership structures, and cross-border asset arrangements.

With more than 15 years of experience advising both U.S. and non-U.S. clients, we provide practical, strategic guidance tailored to each client’s specific circumstances, including coordination with tax advisors, accountants, and foreign counsel where appropriate.

Whether you are reviewing prior filings, addressing foreign account reporting concerns, preparing for expatriation, or evaluating offshore structures, we can help you assess potential risks and develop a clear compliance strategy.

What the IRS’s own ruling tells us about structuring a Foreign Grantor Trust — and why getting this wrong is a multi-million-dollar mistake

You’ve spent a lifetime building wealth. Your children live in the United States. And somewhere along the way, someone told you that transferring that wealth to them — cleanly, efficiently, without losing a significant portion to U.S. taxes — is complicated.

They weren’t wrong. But complicated doesn’t mean impossible. It means you need the right structure — and an attorney who understands exactly how it works.

This article explains one of the most powerful tools available to non-U.S. families with American children: the Foreign Grantor Trust combined with a U.S. Dynasty Trust.

We’ll show you what it does, what problems it solves, and what the IRS itself has confirmed about how it works.

What Problem Does This Solve?

If you are a non-U.S. citizen living outside the United States, and your children or grandchildren are American residents, you face a specific set of challenges that most estate planning attorneys are not equipped to handle:

How do you support your children financially without them paying U.S. income tax on the money they receive?

How do you protect your assets — including U.S. real estate — from U.S. estate tax when you pass away?

How do you ensure your wealth reaches the next generation, and the generation after that, without being eroded by taxes at every step?

How do you buy a home or invest in the U.S. real estate market without inadvertently creating a massive estate tax exposure?

These are real questions that real families face — whether you live in Dubai, São Paulo, Singapore, London, or anywhere else in the world.

And the answer, for many high-net-worth families, is a structure called a Foreign Grantor Trust.

What Is a Foreign Grantor Trust, in Plain English?

A Foreign Grantor Trust is a trust you set up outside the United States — typically in a jurisdiction like the Cayman Islands, BVI, or Liechtenstein — that holds your assets and distributes money to your U.S. children.

Here is the key advantage: because you are a non-U.S. person who retains certain control over the trust, the IRS does not tax the trust’s income.

And when the trust sends money to your children in America, those payments are treated as gifts from you — a non-U.S. person. Which means your children pay no U.S. income tax on those distributions.

Think of it this way. A father living in Hong Kong has $20 million in investments. His two adult children live in New York.

Every year, the trust earns income and distributes $500,000 to each child.

Under a properly structured Foreign Grantor Trust, neither child pays U.S. income tax on that money.

The IRS confirmed this treatment in Private Letter Ruling 200338015, one of the few times the agency has put its reasoning on paper for this type of structure.

What About U.S. Real Estate? Can That Go Into the Trust?

This is the question we hear most often — and the answer surprises most clients. Yes.

U.S. real estate can be held inside a Foreign Grantor Trust. But only if the structure is set up correctly.

Here is the problem with holding U.S. real estate directly.

As a non-U.S. resident, your U.S. estate tax exemption is only $60,000 — compared to over $15 million for U.S. citizens.

That means if you own a $5 million apartment in Manhattan directly, your family could face a $2 million estate tax bill when you die. That is the cost of not planning.

The solution is a foreign blocker corporation.

Instead of the trust owning the U.S. property directly, the trust owns a foreign company (typically a BVI or Cayman entity), which owns the U.S. property.

Because the trust holds foreign company shares — not U.S. real estate directly — those shares are classified as non-U.S. assets for estate tax purposes.

The result: the same Manhattan apartment, owned through the right structure, with zero U.S. estate tax exposure.

IRS PLR 200338015 confirms when gain recognition under Section 684 does and does not apply, clarifying that these rules are limited to transfers to foreign trusts rather than domestications of foreign trusts to U.S. status.

The IRS’s own guidance in PLR 200338015 confirms that when a Foreign Grantor Trust is properly converted to a U.S. Dynasty Trust, the transfer itself “is not treated as a transfer to a foreign trust” — meaning no capital gains tax is triggered, even on assets that have appreciated significantly over the years.

The Big Risk Nobody Talks About: What Happens When You Die?

Here is where most families — and unfortunately, many advisors — get this wrong.

A Foreign Grantor Trust is powerful during your lifetime. But without planning for what happens after your death, it can create a serious tax problem for your children.

When you pass away, the Foreign Grantor Trust loses its special tax status.

If your children then receive distributions from that trust, they can face what is called the throwback tax — a harsh rule that taxes accumulated trust income at the highest rate, plus interest charges for every year that income sat in the trust. Effective tax rates on those distributions can exceed 70%.

The solution is to plan for this before it happens — which is where the second piece of the structure comes in.

The Annual Distribution Rule: Why You Must Distribute Income Every Year

Here is one of the most important practical rules in Foreign Grantor Trust planning — and one that many clients only discover after it is too late to act on it.

Every year that the Foreign Grantor Trust earns income — from investments, rental property, interest, or any other source — that income must be distributed to your U.S. children during your lifetime.

Not most of it. Not eventually. Every year, consistently, before you die.

The reason is straightforward. Any income that the trust earns but does not distribute becomes what the IRS calls Undistributed Net Income (UNI).

UNI sits inside the trust, quietly accumulating. During your lifetime, while you are the foreign grantor, this is not a problem — the trust pays no U.S. tax on it.

But the moment you die and the trust transitions to your children, the IRS activates the throwback rules under IRC §§ 665–668.

At that point, every dollar of UNI that was ever left inside the trust becomes taxable — and the tax bill can be severe.

What the Throwback Tax Actually Costs: A Simple Example

Imagine the trust earns $500,000 per year for 20 years. Each year, rather than distributing that income to your children, the trustee reinvests it inside the trust.

At the end of 20 years, the trust has accumulated $10 million in UNI sitting quietly inside it.

You pass away. The trust transitions to your children. Over the following years, your children begin receiving distributions from the Dynasty Trust. When those distributions are traced back to the $10 million of UNI, the throwback rules apply:

Accumulated UNI over 20 years ($500K/year, not distributed): $10,000,000

Federal income tax on UNI at highest marginal rate (37%): $3,700,000

IRS interest charge on accumulated income (approx., 20 years): $2,200,000+

Total tax cost on $10M of accumulated income: ~$5,900,000+ (59%+ effective rate)

If distributed annually instead — treated as tax-free gifts: $0 tax

The interest charge is particularly punishing.

Unlike regular income tax, which applies once, the IRS calculates interest for each individual year the income sat undistributed in the trust.

Income accumulated in year one carries twenty years of interest charges. Income accumulated in year ten carries ten years.

The longer the trust runs without distributing, the worse the eventual tax bill becomes. It compounds in the wrong direction.

Why Annual Distributions Are Tax-Free to Your Children

This is the part that surprises most clients.

When the Foreign Grantor Trust distributes income to your U.S. children during your lifetime, the IRS treats those distributions as gifts from you — a non-U.S. person.

Gifts from non-U.S. persons to U.S. recipients are not subject to U.S. income tax. Your children pay zero U.S. income tax on those distributions — regardless of the amount.

They do have one obligation: each U.S. child must report every distribution on IRS Form 3520 by April 15 of the following year.

This is a reporting requirement, not a tax return. They are disclosing the gift — not paying tax on it.

Missing this filing, however, triggers a penalty equal to the greater of $10,000 or 35% of the entire distribution amount. On a $500,000 distribution, that is a $175,000 penalty for a missed form.

The Complete Solution: Combining the Foreign Grantor Trust with a U.S. Dynasty Trust

The Foreign Grantor Trust is designed from day one with instructions that, upon your death, all assets transfer automatically into a South Dakota Dynasty Trust — a U.S. trust that holds and grows the family’s wealth for your children, grandchildren, and every generation that follows.

Why South Dakota? Because it is the best trust jurisdiction in the United States. No state income tax. No rule against perpetuities — meaning the trust can last forever.

Some of the strongest creditor protection laws in the country. And a legal framework purpose-built for exactly this kind of multi-generational structure.

When the transition from the Foreign Grantor Trust to the Dynasty Trust is properly structured, the IRS has confirmed in PLR 200338015 that:

There is no capital gains tax on the transfer of assets

There is no gift tax triggered by the conversion

There is no generation-skipping transfer tax on distributions to grandchildren — ever — if the original trust was funded correctly

That last point deserves emphasis.

For U.S. families, transferring wealth to grandchildren requires careful use of the generation-skipping transfer tax exemption — currently about $15 million per person.

For a non-U.S. family that funds the trust correctly from the beginning, the IRS confirmed in PLR 200338015 that “the GST tax does not apply to distributions from and terminations of the Trust” at all.

Not because of an exemption allocation — but because the tax never applies. That is a fundamentally different — and far more powerful — outcome.

One Warning the IRS’s Own Ruling Teaches Us

PLR 200338015 also contains a cautionary lesson buried in its facts.

The grantor in that ruling moved to the United States within five years of setting up the trust.

That single fact triggered a provision of U.S. tax law that immediately treated him as the owner of the trust for U.S. income tax purposes — with full tax obligations from the date of his move.

The IRS confirmed this applied in his case.

The lesson: if you are a non-U.S. client who thinks you might ever move to the United States — for any reason — your trust structure must include a plan for that scenario.

Getting it wrong after the fact is far more expensive than building the contingency in from the start.

Is This Structure Right for Your Family?

A Foreign Grantor Trust combined with a U.S. Dynasty Trust is not for everyone. It is most valuable when:

You are a non-U.S. citizen or resident with significant assets outside the United States

You have children, grandchildren, or other beneficiaries who live in the U.S.

You own or want to own U.S. real estate, U.S. investments, or U.S. business interests

You want to protect your wealth from creditors, lawsuits, and divorce proceedings

You want your family’s wealth to last for multiple generations — not just your children’s lifetimes

You are considering moving to the United States and want to plan before you arrive

If any of these describe your situation, the structure is worth exploring with an attorney who specializes in exactly this area.

The compliance requirements are real — your U.S. children will need to file annual reports with the IRS, and missing a filing can trigger significant penalties.

But with the right team in place, this structure runs smoothly and delivers exactly what it promises.

Work With Max Dilendorf

Max Dilendorf is an attorney at Dilendorf Law Firm, based in New York.

He represents domestic and international high-net-worth families and individuals across a broad range of matters, including cross-border tax planning, foreign trust structuring, U.S. Dynasty Trust formation, pre-immigration planning, and asset protection strategies.

Max also represents clients navigating complex cybersecurity incidents and advises individuals and families on building asset protection plans designed for the digital age — including the protection and proper structuring of cryptocurrency and other digital assets.

Whether your family is based abroad, you are planning a move to the United States, or you are managing wealth across multiple jurisdictions and asset classes — Max and his team can help you build a structure that works.

Can a non-US parent set up a trust for US children without paying US gift tax?

Yes — if the trust holds non-U.S. assets. The IRS confirmed in PLR 200338015 that a non-resident alien who transfers non-U.S. situs assets to a foreign trust does not trigger U.S. gift tax. The assets are outside the U.S. gift tax system entirely.

What happens to the trust when the foreign parent dies?

Without planning, the trust loses its favorable tax status and the children can face severe throwback taxes. With proper planning, the assets pour over into a U.S. Dynasty Trust with no capital gains tax, no gift tax, and no generation-skipping transfer tax — as confirmed by IRS PLR 200338015.

Can I buy real estate in New York or Miami through a Foreign Grantor Trust?

Yes — through a foreign blocker corporation that sits between the trust and the U.S. property. This structure converts a U.S. situs asset into non-U.S. situs stock, eliminating estate tax exposure for non-U.S. residents.

Do my children have to pay tax on money they receive from the trust?

No — during the grantor’s lifetime, distributions from a Foreign Grantor Trust to U.S. beneficiaries are treated as gifts from a foreign person. U.S. beneficiaries report them on Form 3520 but pay no U.S. income tax on the amounts received.

Resources

Foreign Grantor Trust — Governing Statutes

26 U.S.C. § 671 — Grantor Treated as Substantial Owner

https://www.law.cornell.edu/uscode/text/26/671

26 U.S.C. § 672(f) — Special Rule for Foreign Grantors

https://www.law.cornell.edu/uscode/text/26/672

26 U.S.C. § 675(4) — Power to Substitute Assets (Swap Power)

https://www.law.cornell.edu/uscode/text/26/675

26 U.S.C. § 676 — Power to Revoke Trust

https://www.law.cornell.edu/uscode/text/26/676

26 U.S.C. § 679 — Foreign Trusts with U.S. Beneficiaries; Five-Year Residency Rule

https://www.law.cornell.edu/uscode/text/26/679

26 U.S.C. § 684 — Recognition of Gain on Transfers to Foreign Trusts

https://www.law.cornell.edu/uscode/text/26/684

26 U.S.C. § 7701(a)(30)(E) — Definition of Foreign Trust

This article is for general informational and educational purposes only. It does not constitute legal or tax advice and does not create an attorney-client relationship. Tax laws change, and individual circumstances vary. Please consult qualified U.S. international tax and estate planning counsel before taking any action.

The Theft Takes 10 Minutes. The Damage Can Last Years.

A domain name is not just a web address.

For most businesses, it is the front door to their entire digital operation — their email infrastructure, customer portal, e-commerce platform, and brand identity, all anchored to a string of characters registered with a hosting provider.

When that domain is stolen, everything connected to it can be weaponized, redirected, or destroyed within hours.

Domain account takeovers are among the fastest-moving cybercrime events that attorneys encounter.

According to the FBI’s IC3, U.S. cybercrime losses hit a record $20.9 billion in 2025, led by business email compromise and account takeover schemes.

Domain hijacking sits at the intersection of both.

What makes domain takeover cases uniquely devastating is the speed.

A skilled attacker with access to a registrar account can transfer a domain, reroute DNS records to offshore servers, and disable two-factor authentication recovery options in under 10 minutes.

Global DNS propagation — the process by which the new, fraudulent routing instructions spread across the internet — can complete within 24 to 48 hours, sometimes sooner.

By the time a business owner realizes what has happened, their domain may already be resolving to a fraudulent website hosted in a jurisdiction with no U.S. law enforcement cooperation.

This is not a hypothetical. It is a documented, repeatable attack pattern that affects thousands of businesses every year.

Who Is Doing This — and How

Federal law enforcement and cybersecurity researchers have identified several well-documented methods attackers use to execute domain account takeovers.

Understanding the attack vector matters because it directly shapes how victims and their attorneys build a legal case and pursue recovery.

SIM-Swap Attacks remain the most prevalent gateway to domain takeover.

The attacker contacts a mobile carrier — Verizon, AT&T, T-Mobile — impersonates the victim, and convinces a customer service representative to port the victim’s phone number to a SIM card under the attacker’s control.

Once they control the phone number, they reset the registrar account password using SMS-based two-factor authentication.

The Federal Communications Commission (FCC) has issued specific consumer guidance on SIM-swapping, acknowledging it as a systemic vulnerability in carrier identity verification protocols.

The FCC’s rules, updated in 2023, now require carriers to implement additional authentication before processing SIM transfers — but enforcement remains inconsistent.

Phishing and Credential Stuffing account for a significant portion of direct registrar account compromises.

Credential stuffing — using previously leaked username and password combinations against registrar login portals — is particularly effective against account holders who reuse passwords across platforms.

Social Engineering of Registrar Support Staff is a documented attack vector that has been used against major registrars including GoDaddy.

In 2020, GoDaddy publicly confirmed that a social engineering attack against its customer support staff resulted in unauthorized changes to domain settings for multiple cryptocurrency exchange domains, including liquid.com and NiceHash.

The attackers did not need technical access — they needed a convincing story and a support agent willing to bypass verification protocols.

Insider Threats and Unauthorized Employee Access represent a less frequently discussed but legally significant category.

Former employees with residual access credentials, or third-party IT vendors with administrative access, can execute domain transfers that are indistinguishable from legitimate account activity in the initial logs.

The Major Registrars Where Takeovers Occur

Max Dilendorf and the team at Dilendorf Law Firm represent individuals and businesses who have been victims of domain account takeovers across the largest registrar platforms in the United States, including:

GoDaddy — the world’s largest domain registrar, hosting over 84 million domain names globally

Register.com — one of the oldest U.S. registrars, now operated under the Web.com Group

Namecheap — a major registrar with over 17 million registered domains

Network Solutions — a legacy registrar widely used by enterprise and government clients

Cloudflare Registrar — increasingly used by sophisticated businesses for its DNS management capabilities

Each of these platforms maintains its own security protocols, account recovery procedures, and — critically — its own terms of service governing dispute resolution.

GoDaddy and Register.com, for example, include binding mandatory arbitration clauses in their terms of service.

This means disputes between a domain holder and the registrar — over security failures, negligence in identity verification, or unauthorized transfers — may bypass federal and state courts entirely.

Instead, they proceed through private arbitration forums such as the American Arbitration Association (AAA), JAMS, and the National Arbitration and Mediation forum (NAM).

Understanding the contractual framework governing your registrar relationship is not optional. It is the foundation of your legal strategy.

Max Dilendorf: Digital Asset and Cybercrime Attorney Since 2017

Max Dilendorf has represented digital asset holders, businesses, and high-net-worth individuals in cybercrime and account takeover matters since 2017.

He is among the earliest U.S. attorneys to practice at the intersection of digital asset law and cybercrime enforcement.

His arbitration experience spans some of the most complex digital asset loss cases in the United States.

He has arbitrated 130+ matters at AAA, JAMS, and NAM against financial institutions, digital asset custodians, and telecommunications carriers for breach of contract, gross negligence, and breach of fiduciary duty.

These cases share a common thread: an institution’s failure to implement adequate security controls resulted in a victim’s irreversible financial loss — and the victim’s only path to recovery ran through a binding arbitration clause buried in a terms of service agreement.

Domain account takeover cases follow the same legal architecture.

GoDaddy’s support staff is required to verify identity before making any account changes. Register.com’s authentication systems are expected to flag unauthorized logins from anomalous IP addresses.

When either fails, those failures may constitute actionable breaches of the registrar’s contractual obligations and duty of care to the account holder.

What separates successful recovery cases from failed ones is almost always the same factor: how quickly the victim engaged qualified legal counsel and how completely the evidentiary record was preserved in the hours and days immediately following the attack.

Dilendorf’s Team Behind the Investigation

Dilendorf Law Firm’s domain takeover practice is supported by a team that includes retired FBI and Department of Justice cybercrime enforcement agents who bring direct investigative experience to private matters.

This matters for several reasons that go beyond legal credentials.

Former federal agents know exactly how law enforcement triages cybercrime complaints.

That experience matters when filing your IC3 report. A properly structured report significantly increases the probability that the FBI’s Cyber Division or a regional USSS Electronic Crimes Task Force will open an active investigation.

They understand the investigative timelines, the evidentiary standards that federal prosecutors require, and the specific technical documentation that makes a case actionable.

They also understand what registrars and hosting providers are capable of producing — and what they will resist producing without legal compulsion.

Account access logs, login IP history, security audit logs, and internal support ticket records are critical evidence in domain takeover cases.

These records are not always preserved indefinitely.

Engaging counsel immediately creates the legal basis for a preservation demand letter — a formal written instruction to the registrar requiring them to preserve all relevant records pending litigation or arbitration.

The First 48 Hours: A Step-by-Step Response Framework

The actions a victim takes — or fails to take — in the first 48 hours after a domain takeover are the single most determinative factor in whether recovery is possible.

Here is the framework Max Dilendorf’s team follows with new clients:

Hour 1–2: Confirm and Document the Takeover

Do not attempt to log into your registrar account repeatedly.

Failed login attempts can trigger account lockouts that complicate recovery.

Instead, use a WHOIS lookup tool — ICANN’s WHOIS database is publicly accessible at lookup.icann.org — to confirm whether the registrant information on your domain has been changed. Screenshot everything.

Document the current DNS records. Note the exact time you discovered the compromise.

Hour 2–4: Contact the Registrar’s Abuse and Security Team

Every major registrar maintains a separate abuse or security escalation contact that operates independently from standard customer support.

Do not call the general customer service line.

For GoDaddy, the relevant contact is their abuse reporting channel.

For Network Solutions and Register.com, escalation paths exist through their legal and security departments.

Request an immediate account freeze and preservation of all account activity logs. Put this request in writing — email creates a timestamped record.

Hour 4–6: File an IC3 Report

The FBI’s Internet Crime Complaint Center at ic3.gov is the mandatory first step for federal law enforcement engagement.

Filing takes under 10 minutes if you have your documentation prepared.

The report should include: your domain name, the registrar, the approximate time of the compromise, any known attack vector (SIM-swap, phishing, etc.), estimated financial damages, and any associated business email compromise.

The quality and completeness of your IC3 report directly affects whether the FBI’s Cyber Division assigns an agent to your case.

A vague, incomplete report is far less likely to generate active federal investigation.

Hour 6–12: File with CISA and FTC

CISA maintains a reporting portal at cisa.gov/report for cybersecurity incidents.

The Federal Trade Commission accepts identity theft and account takeover reports at reportfraud.ftc.gov.

These filings create additional federal records and may trigger parallel agency involvement, particularly if the attack involved a telecommunications carrier in a SIM-swap.

Hour 12–24: Engage Cybercrime Counsel and Issue Preservation Demands

This is where legal counsel becomes not just advisable but essential.

An experienced cybercrime attorney can immediately issue preservation demand letters to the registrar, any involved telecommunications carrier, and any hosting provider where DNS records were redirected.

These letters are legally significant — they place the recipient on formal notice that litigation or arbitration is anticipated and that destruction of relevant records may constitute spoliation of evidence.

Hour 24–48: Evaluate Emergency Relief Options

Depending on the circumstances, emergency legal relief may be available through federal court in the form of a temporary restraining order (TRO) compelling the registrar to freeze the domain transfer and restore access pending a full hearing.

These applications are time-sensitive, fact-intensive, and require experienced counsel to execute effectively. Not every case qualifies — but for high-value domains where irreparable harm can be demonstrated, emergency injunctive relief can be the fastest path to restoration.

The Evidence That Wins These Cases

Experienced cybercrime attorneys know that domain takeover cases are built on technical evidence that most victims do not know exists — and that registrars do not volunteer.

The critical evidence categories include:

Account Access Logs — A timestamped record of every login, failed login, and session initiation associated with the registrar account.

These logs can establish exactly when unauthorized access occurred and from which IP address.

Login IP History — The specific IP addresses used to access the account before, during, and after the takeover.

Anomalous IP addresses — particularly those geolocated to foreign jurisdictions or associated with known VPN or proxy services — are powerful evidence of unauthorized access.

Security Audit Logs — Records of every security-relevant action taken on the account: password changes, two-factor authentication modifications, authorized contact updates, and domain transfer initiations.

These logs tell the story of the attack in sequential detail.

Support Ticket and Chat Records — Internal records of any customer support interactions associated with the account during the attack window.

In social engineering cases, these records may directly capture the fraudulent representations made by the attacker to support staff.

DNS Change Logs — Records showing when DNS records were modified and what values were substituted.

These logs establish where the domain was redirected and provide technical evidence for tracing the attacker’s infrastructure.

Obtaining these records requires formal legal process — either a preservation and production demand backed by arbitration or litigation authority, or a subpoena issued through federal court in connection with an active criminal investigation.

This is why engaging counsel in the first 48 hours is not a recommendation. It is a requirement.

Most domain registrar agreements — including GoDaddy and Register.com — contain mandatory binding arbitration clauses that require disputes to be resolved through private arbitration rather than civil litigation.

For victims, this has both advantages and disadvantages.

The advantage is speed.

Why Arbitration Changes Everything

Arbitration proceedings at AAA, JAMS, and NAM move significantly faster than federal court litigation.

Emergency relief mechanisms exist within arbitration frameworks that can be invoked quickly.

Arbitration also tends to produce less public exposure — a consideration for businesses concerned about reputational harm from a publicly filed lawsuit.

The disadvantage is that arbitration requires experienced counsel who understands the procedural rules of each forum, the discovery mechanisms available within arbitration, and the specific claims — breach of contract, gross negligence, violations of federal and state consumer protection laws — that registrar defendants are most vulnerable to.

Filing an arbitration claim without this expertise is likely to result in dismissal or an inadequate award.

Max Dilendorf has arbitrated complex cybercrime cases across all three major forums — AAA, JAMS, and NAM — against financial institutions, digital asset custodians, and telecommunications carriers.

His team understands the precise legal architecture of these cases and how to build the evidentiary record that arbitration panels find compelling.

Contact Dilendorf Law Firm

If your domain has been compromised, or if you believe you are at risk, time is the most critical variable in your case.

The longer evidence goes unpreserved, the narrower your legal options become.

This article is for informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship. If you have experienced a domain account takeover, contact a qualified cybercrime attorney immediately.

[Attorney Advertising]

U.S. Exit Tax Rules and Expatriation Planning

Leaving the United States – whether by renouncing citizenship or relinquishing a Green Card – is not merely a lifestyle decision.

Without proper planning, it can trigger significant and unexpected tax consequences.

This is not just about booking a ticket and moving abroad, it is about navigating a complex tax framework that requires careful, proactive planning.

Timing is critical. Clients who begin planning close to expatriation often face limited flexibility and fewer effective strategies.

In some cases, the act of expatriation alone can create a multi-million-dollar tax obligation without any actual sale of assets.

Expatriation is a legal event. Exit is a strategy. Confusing the two is where many costly mistakes begin.

A Sale That Never Happened – But Still Taxed

The U.S. exit tax regime, governed by 26 U.S.C. § 877A, treats expatriation as a taxable event.

In many cases, individuals are deemed to have sold their worldwide assets at fair market value on the day before expatriation.

This includes business interests, real estate, and digital assets.

Any gain arising from this deemed sale is included in income for that tax year, regardless of whether the assets were actually sold. SeeI.R.S. Notice 2009-85, 2009-45 “[A]ll property of a covered expatriate is treated as sold on the day before the expatriation date for its fair market value.”

As the Supreme Court has recognized, “realization of gain need not be in cash derived from the sale of an asset” Helvering v Bruun, 309 US 461, 469 [1940]

Consistent with this principle, the Tax Court has confirmed that “[a]s a covered expatriate petitioner is treated as having sold all his property on the day before his expatriation date and is subject to income tax on the net unrealized gain arising from property deemed sold while he was still a U.S. [lawful permanent resident]” Topsnik v Commissioner, 146 TC 1, 13-14 [2016]

As a result, significant tax liability may arise even where no actual sale has occurred. Careful planning is essential to manage this exposure.

Covered Expatriate Status Under IRS Guidance

Not every individual who relinquishes U.S. citizenship or a Green Card is subject to the exit tax. The key determination is whether the individual is classified as a “covered expatriate”.

Under Internal Revenue Service (IRS) guidance interpreting 26 U.S.C. § 877A, individuals who expatriate may be classified as “covered expatriates” if they meet certain criteria.

This classification is based on three (3) independent tests, each of which can trigger exit tax exposure on its own. Understanding how these tests operate is critical, as many individuals meet one of them without realizing it.

Test

What It Measures

Key Risk

Net Worth Test

Total worldwide net worth at time of expatriation (threshold: $2 million)

Clients often underestimate asset values, especially private businesses and cryptocurrency

Tax Liability Test

Average annual U.S. income tax liability over the prior 5 years (adjusted annually)

High earners may qualify even without substantial net worth

Compliance Test

Full compliance with U.S. tax and reporting obligations for the prior 5 years

Technical reporting failures (FBAR, FATCA) can trigger covered expatriate status

Importantly, these tests operate independently: meeting any one of them is sufficient to trigger covered expatriate status.

Many individuals assume that only ultra-high-net-worth taxpayers are affected; however, IRS guidance makes clear that income levels and compliance history alone may result in this classification.

With respect to compliance, “a penalty of up to $100,000 or 50% of the balance of the account at the time of the violation, whichever is greater, for failures to file an FBAR as required by 26 U.S.C. § 5314” See Crawford v United States Dept. of the Treasury, 2015 US Dist LEXIS 131496, at *45, 116 A.F.T.R.2d (RIA) 2015-6288 [SD Ohio Sep. 29, 2015, No. 3:15-cv-250]

Pre-Expatriation Planning Strategies

Once an individual is classified as a covered expatriate, the ability to mitigate exit tax exposure becomes significantly limited.

As a result, planning must occur before expatriation is initiated. Effective strategies depend on timing, asset composition, and prior tax compliance. These may include, but are not limited to:

Net Worth Management – evaluating global asset values and exposure relative to applicable thresholds

Income and Tax Liability Analysis – reviewing historical tax liability and timing of income recognition

Compliance Review – confirming full compliance with U.S. tax filings and international reporting (including FBAR and FATCA)

Digital Assets Considerations – assessing valuation, reporting, and unrealized gains in cryptocurrency holdings

Pre-Expatriation Gifting and Structuring – considering transfers or restructuring prior to expatriation

State Tax Exit Planning – addressing domicile and residency risks in jurisdictions such as New York and California

When implemented early, these strategies can materially reduce overall tax exposure.

Contact Us

Dilendorf Law Firm advises clients on U.S. exit tax planning, expatriation strategies, and cross-border structuring, including analysis under 26 U.S.C. § 877A.

We assist with pre-expatriation planning, review of prior tax filings, and preparation of required reporting, including Form 8854 and related disclosures.

Our practice also includes estate planning and asset protection strategies, including the formation of domestic and international trust structures designed to align with clients’ long-term tax, succession, and wealth preservation goals.

We regularly work with high-net-worth individuals, entrepreneurs, and international families navigating complex cross-border issues.

With more than 15 years of experience advising both U.S. and non-U.S. clients, our firm provides practical, strategic guidance tailored to each client’s specific circumstances, including coordination with tax advisors, accountants, and foreign counsel where needed.

Whether you are considering expatriation, reviewing your compliance history, or structuring your assets in advance, we can help you evaluate your options and develop a clear plan.

One governs Controlled Foreign Corporations (CFCs). The other governs Passive Foreign Investment Companies (PFICs).

These rules are complex. Mistakes are costly. Penalties often start at $10,000 per form per year. In many cases, the statute of limitations stays open until the form is filed.

This article explains how these regimes work. It also explains when they apply and how stock options are treated.

It also includes domestic entities such as corporations and trusts.

Visa holders must apply the substantial presence test under IRC § 7701(b).

This test counts days spent in the United States over a three-year period.

Some visa holders receive special treatment. F-1 and J-1 visa holders may qualify as “exempt individuals.”

During this time, they are not treated as U.S. tax residents.

This exemption is temporary.

Once it ends, worldwide reporting begins. This includes Forms 5471 and 8621 if foreign interests exist.

Other visa holders do not receive this benefit. H-1B, L-1, O-1, E-2, and TN holders often become tax residents quickly.

Once you are a U.S. person, global reporting rules apply.

Two Different Regimes

U.S. tax law uses two main systems for foreign corporations.

These are the CFC rules and the PFIC rules.

Both aim to prevent tax deferral.

However, they apply in very different ways. Understanding the difference is essential.

Controlled Foreign Corporations (CFCs)

A foreign corporation is classified as a CFC when U.S. ownership exceeds 50 percent.

Each relevant U.S. shareholder must own at least 10 percent.

The 10 percent threshold is critical.

If no U.S. person owns 10 percent or more, Form 5471 usually does not apply.

Example: CFC Classification

A U.S. entrepreneur forms a company in India and owns 100 percent of it. This company is a CFC. The owner must file Form 5471 every year.

In another example, three U.S. investors each own 20 percent of a foreign startup. Together, they own 60 percent. Each investor exceeds the 10 percent threshold. The company is a CFC, and all three investors must file Form 5471.

Even changes in ownership can trigger reporting. For example, if a U.S. shareholder sells shares and drops below 10 percent, a final Form 5471 may still be required.

Passive Foreign Investment Companies (PFICs)

The PFIC rules focus on income and assets, not ownership percentage.

As the IRS provides, a foreign corporation can be deemed a PFIC for any taxable year if (1) at least 75 percent of its gross income for the taxable year is passive income or (2) at least 50 percent of the value, determined on the basis of a quarterly average, of its assets produce or are held to produce passive income, like dividends, interest, royalties or rents.

Passive income includes dividends, interest, and investment gains.

There is no minimum ownership threshold. Even a very small investment may trigger Form 8621.

Example: PFIC Classification

A U.S. taxpayer invests in an Australian or Canadian mutual fund.

The fund earns mostly dividends and capital gains.

It meets the PFIC income test. The taxpayer must file Form 8621 each year.

In another case, a U.S. individual buys shares in a European ETF.

The ETF holds passive investment assets. It qualifies as a PFIC. Even a small investment triggers reporting.

A third example involves inheritance.

A U.S. person inherits 3 percent of a foreign holding company. The company mainly holds stocks and securities.

It meets the PFIC tests. Form 8621 is required despite the small ownership.

Stock Options: A Key Difference

Stock options are treated differently under each regime.

Under CFC rules, options usually do not count as ownership. They count only after exercise.

Under PFIC rules, options are treated as ownership. This rule comes from IRC § 1298(a)(4).

IRC § 1298(a)(4) provides that:

“[t]o the extent provided in regulations, if any person has an option to acquire stock, such stock shall be considered as owned by such person. For purposes of this paragraph, an option to acquire such an option, and each one of a series of such options, shall be considered as an option to acquire such stock.”

Example: Stock Options in Practice

A U.S. employee receives options to acquire 10 percent of a foreign startup.

Under CFC rules, the options do not count until exercised.

The employee may not have Form 5471 filing obligations yet.

Under PFIC rules, the options are treated as owned stock.

If the company qualifies as a PFIC, the employee may need to file Form 8621 immediately.

This difference creates real risk.

A taxpayer may believe no reporting is required, while PFIC rules already apply.

Attribution Rules Expand Ownership

Ownership is not limited to shares held directly.

U.S. tax law uses attribution rules to expand ownership.

These rules include shares owned by family members and related entities.

This includes spouses, children, parents, partnerships, and trusts.

For Form 5471, siblings are also included.

Example: Attribution Rules

A U.S. taxpayer owns 6 percent of a foreign company. Their child owns 8 percent. The taxpayer is treated as owning 14 percent.

This exceeds the 10 percent threshold. Form 5471 is required.

In another case, two siblings each own 6 percent of a foreign corporation. Each sibling is treated as owning 12 percent. Both must file Form 5471.

These rules often create unexpected filing obligations.

When Form 5471 Is Required

Form 5471 is required when certain ownership thresholds or events occur.

Under IRC § 6046(a)(1), a U.S. person must file if they acquire stock representing “10 percent or more of the total combined voting power of all classes of stock entitled to vote, or 10 percent or more of the total value of shares of all classes of stock” in a foreign corporation.

Filing is also required if the person controls the corporation, which usually means owning more than 50 percent.

A filing obligation also exists if the taxpayer is a 10 percent shareholder in a CFC at the end of the year.

Changes in ownership matter as well. Selling shares and dropping below 10 percent can still trigger reporting.

Example: Form 5471 Trigger

A U.S. investor acquires 12 percent of a foreign company during the year.

Even if the shares are later sold, a Form 5471 filing may still be required for that year.

When Form 8621 Is Required

Form 8621 is triggered by events rather than ownership levels.

A taxpayer must file if they receive a distribution from a PFIC.

Filing is also required if they sell PFIC stock or recognize gain.

Filing is also required when certain elections are made or maintained.

Each PFIC requires a separate form. This can create a large compliance burden.

Example: Form 8621 Trigger

A U.S. taxpayer owns shares in a foreign mutual fund. The fund pays a dividend during the year. This triggers a Form 8621 filing.

In another case, a taxpayer sells shares in a PFIC at a gain. This also triggers reporting.

Even without activity, annual reporting may still be required in some cases.

When Both Rules Apply

Some companies qualify as both CFCs and PFICs.

In these cases, the rules interact. CFC rules generally take priority for shareholders who own at least 10 percent.

Smaller shareholders may still be subject to PFIC rules.

Example: Overlap Scenario

A foreign company is owned 60 percent by U.S. shareholders. One shareholder owns 15 percent. Another owns 5 percent.

The 15 percent shareholder follows CFC rules and files Form 5471.

The 5 percent shareholder does not meet the 10 percent threshold. That shareholder may still need to file Form 8621 if the company qualifies as a PFIC.

This creates different reporting obligations for investors in the same company.

Penalties Are Significant

Penalties for noncompliance are severe.

Form 5471 penalties start at $10,000 per year. Additional penalties may apply if the failure continues.

“A $10,000 penalty is imposed for each annual accounting period of each foreign corporation for failure to furnish the information required by section 6038(a) within the time prescribed. If the information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof, during which the failure continues after the 90-day period has expired.”

Form 8621 penalties can also be substantial. In addition, the PFIC tax regime can impose high tax rates and interest charges.

The statute of limitations may remain open until forms are filed.

Planning Options Exist

Some planning tools are available to reduce risk.

Under PFIC rules, taxpayers may make a Qualified Electing Fund (QEF) election. They may also make a mark-to-market election.

Under CFC rules, individuals may consider a Section 962 election.

Example: Planning Opportunity

A taxpayer holding PFIC shares may make a QEF election early. This can avoid punitive tax treatment later when the shares are sold.

Planning must be done carefully. Timing and documentation are critical.

Conclusion

CFC and PFIC rules are complex but different.

CFC reporting depends on ownership thresholds.

Stock options usually do not count until exercised.

PFIC reporting applies broadly. It applies even at low ownership levels. Stock options are treated as ownership.

These differences can create unexpected obligations. Careful analysis is required in every case.

Contact Us

If you hold foreign investments, you should seek legal guidance.

This is especially important for complex ownership structures and stock options.

Max Dilendorf, from Dilendorf Law Firm, represents U.S. and non-U.S. clients with:

Planning around and optimizing taxes under CFC and PFIC rules

In addition, Max Dilendorf assists clients with reviewing and drafting non-willful conduct statements.

These statements are critical in streamlined submissions and must be prepared carefully to withstand IRS scrutiny.

Contact Dilendorf Law Firm to discuss your situation and ensure full compliance.

Phone: 212.457.9797 | Email: max@dilendorf.com

Disclaimer

Nothing in this article constitutes legal or tax advice. This content is provided for informational and educational purposes only. You should consult a qualified attorney or tax advisor regarding your specific situation.

Domestic Asset Protection Trusts, or DAPTs, are often promoted as powerful tools for protecting wealth from future creditors. Alaska was one of the first states to authorize these self-settled trusts, and its statute is frequently cited in asset protection planning.

But Battley v. Mortensen (In re Mortensen), 2011 Bankr. LEXIS 5004 (Bankr. D. Alaska Jan. 14, 2011) shows that state-law compliance is only part of the analysis. In bankruptcy, the transfer into a DAPT may still be challenged under federal law, and a properly formed trust can remain vulnerable if the surrounding facts suggest fraudulent intent.

The Facts Behind the Dispute

In Mortensen, the debtor created an Alaska asset protection trust in February 2005 and transferred into it real property located in Seldovia, Alaska.

The trust beneficiaries included the debtor and his descendants. The trust instrument stated that its purpose was: “to maximize the protection of the trust estate or estates from creditors’ claims of the Grantor or any beneficiary and to minimize all wealth transfer taxes.” Id. at 2.

At the time of the transfer, the debtor had credit card debt but no pending or threatened litigation.

According to the decision, he later accumulated substantially more debt and eventually filed for Chapter 7 relief in 2009. The chapter 7 trustee then brought an adversary proceeding seeking to recover the transferred property as a fraudulent conveyance.

Why This Case Matters

The significance of Mortensen is not simply that the debtor used an Alaska DAPT. The important point is that the bankruptcy court treated the trust as subject to a separate federal fraudulent transfer analysis.

The court explained that the trustee was proceeding under 11 U.S.C. § 548(e), a provision added in 2005.

According to the court, § 548(e): “closes the self-settled trusts loophole” and was directed at the five states that permitted such trusts, including Alaska.

That statement is one of the most frequently cited passages from the case, and for good reason. It confirms that Congress specifically addressed self-settled asset protection trusts in bankruptcy and gave trustees a targeted tool to challenge them.

State DAPT Law Does Not Control the Bankruptcy Result

One of the debtor’s core arguments was that the trust was valid under Alaska law. The court rejected the idea that this, by itself, resolved the dispute. It stated plainly:

“[…] the fact that Mortensen’s trust complies with Alaska law will not protect it from avoidance if the trustee can establish all of the elements of § 548(e).” Id. at 7.