At Dilendorf Law Firm, we establish and administer Cook Islands and Nevis offshore asset protection trusts for U.S. and international clients seeking the strongest available creditor protection, privacy, and multigenerational wealth preservation.

These two jurisdictions are widely regarded as the most protective trust jurisdictions in the world.

Both refuse to recognize most foreign judgments, both apply a criminal-standard burden of proof to fraudulent-transfer claims, and both maintain short statutes of limitations that foreign creditors rarely meet.

Properly structured, a Cook Islands or Nevis trust can hold cash, investments, real estate, business interests, and digital assets — without requiring the assets to physically reside in the jurisdiction.

If you are considering an offshore trust as part of a long-term asset protection plan, contact us at info@dilendorf.com or 212.457.9797 for a confidential consultation.

ATTORNEYS' EXPERIENCE

ATTORNEYS' EXPERIENCE

We structure offshore asset protection trusts for family offices, crypto portfolio managers, business owners, foreign investors, and founders — including hybrid structures with offshore LLCs, Swiss or Liechtenstein custody, and U.S. domestic feeder trusts.

The Cook Islands’ International Trusts Act 1984 was the first modern asset-protection trust statute and remains the model that most other jurisdictions imitate.

Nevis followed with the International Exempt Trust Ordinance in 1994 (substantially amended in 2015 and 2020), adopting and in some respects expanding on the Cook Islands framework.

Both jurisdictions share the protective features that make them genuinely different from U.S. domestic trusts:

Non-recognition of foreign judgments. A U.S. creditor cannot enforce a U.S. judgment against trust assets — the creditor must re-litigate the entire claim locally, in person, under local law.

Criminal-standard burden of proof. Creditors must prove fraudulent transfer beyond a reasonable doubt — the same standard used in criminal prosecutions, far higher than the preponderance standard used in U.S. civil courts.

Short statutes of limitations. Fraudulent-transfer claims must generally be brought within one to two years of the transfer, with the burden of proof on the creditor.

Nevis bond requirement. Nevis statutorily requires a creditor to post a $100,000 bond before filing suit, screening out speculative claims; the Cook Islands does not impose a statutory bond but the practical cost of local litigation creates a similar deterrent.

No forced heirship. Foreign forced-heirship rules cannot reach trust assets.

Confidentiality. Trust ownership details are statutorily protected, and unauthorized disclosure of trust information is a criminal offense in Nevis.

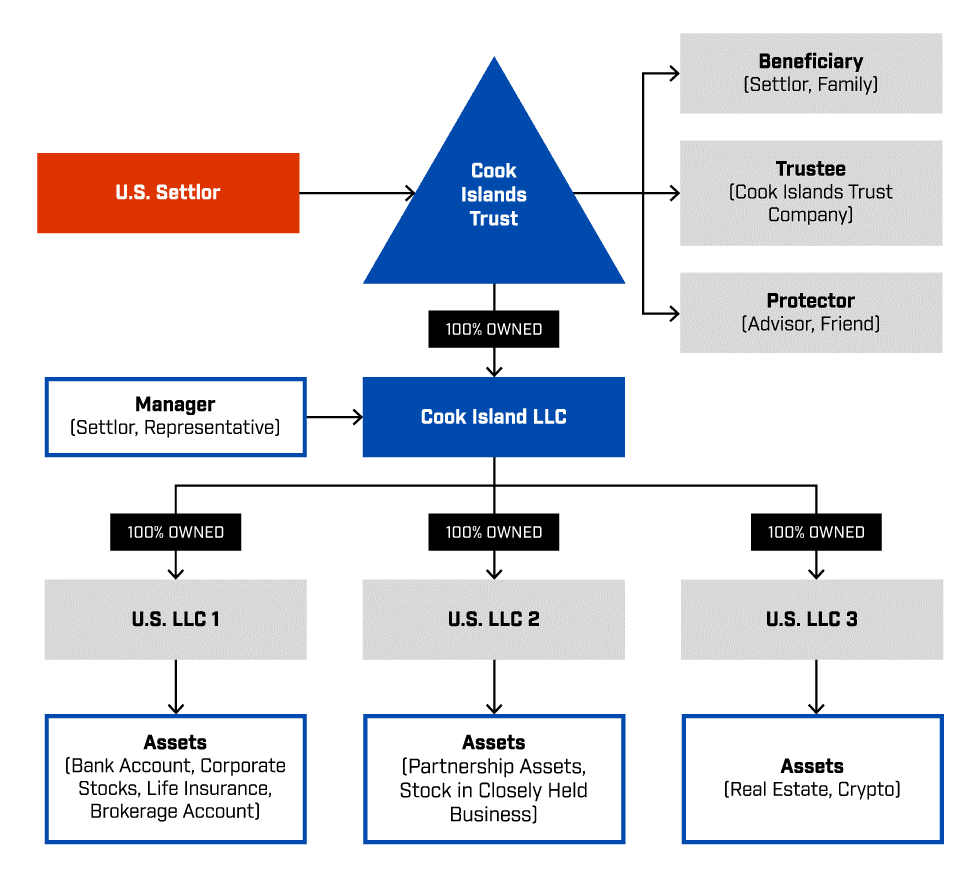

How the Structure Works

A typical offshore asset protection trust pairs the trust with an underlying limited liability company (LLC) registered in the same or another jurisdiction.

This separates legal title (held by the offshore trustee) from operational control (held by the settlor or the settlor’s designated manager).

The settlor establishes the trust under Cook Islands or Nevis law.

A licensed offshore trustee in the jurisdiction holds legal title to the trust assets.

The settlor and family members are typically appointed discretionary beneficiaries.

A protector — often a U.S. advisor close to the family — can be appointed to monitor the trustee and hold veto or removal powers.

The trust owns 100% of an LLC that holds the operating assets; the settlor or a representative manages the LLC day-to-day.

The settlor provides a letter of wishes guiding the trustee’s discretion during and after the settlor’s lifetime.

A duress clause in the trust deed instructs the trustee to refuse repatriation orders made under foreign court pressure.

In normal circumstances, the trustee does not interfere with management. The structure activates fully — the trustee asserts control, refuses U.S. court orders, and protects the assets — only under duress.

Cook Islands vs. Nevis — Practical Differences

Both jurisdictions provide world-class protection. The choice between them turns on case-specific factors.

Cook Islands is the most case-tested jurisdiction with four decades of court precedent affirming the regime’s resilience against U.S. enforcement efforts. Strongest fit for clients prioritizing legal predictability and the deepest professional infrastructure.

Nevis offers a comparable statutory framework with the added barrier of the $100,000 statutory bond and a generally lower cost structure. Strongest fit for clients prioritizing cost efficiency and the deterrent value of the bond hurdle.

We assess both jurisdictions against the client’s risk profile, asset mix, and long-term objectives — and in many cases recommend a hybrid structure layering the offshore trust with a U.S. domestic asset protection trust (Wyoming, Nevada, or South Dakota) as an additional barrier.

Asset Types We Structure For

Liquid investments — held through Swiss or Liechtenstein custody, or through U.S. brokerage accounts under appropriate structuring

Digital assets and cryptocurrency — including direct holding by the offshore LLC, custody through licensed digital-asset custodians, and integration with crypto special-purpose trusts

Real estate — U.S. and international, held through the underlying LLC or feeder entities

Business interests — operating company shares, LLC membership interests, and intellectual property

Premarital and inherited assets — preserved as separate property through proper trust drafting

Important Considerations

Offshore trusts are a legitimate, court-recognized planning tool — but they are not for every client and must be structured correctly.

Timing matters. A trust established before any threat of litigation is effective. A trust funded after a claim has arisen — or in anticipation of one — can be unwound under U.S. fraudulent-transfer law and may expose the settlor to contempt sanctions, including in some cases incarceration for failure to repatriate assets.

Full U.S. tax reporting is required. A properly structured offshore asset protection trust is tax-neutral — it does not avoid U.S. income tax. Settlors must comply with IRS Form 3520 and Form 3520-A foreign-trust reporting, FBAR (FinCEN 114), and Form 8938 FATCA reporting where applicable.

OFAC and AML compliance. Offshore trustees apply rigorous due diligence; clients should expect detailed source-of-funds documentation.

Not for hiding assets. The strength of these structures comes from substantive law and procedural barriers — not concealment. Reportable interests must be reported.

Why Engage Counsel

U.S. courts have spent more than four decades scrutinizing offshore asset protection trusts. Many of the published “trust failure” cases involve do-it-yourself structures, trusts funded too late, or settlors who retained too much control.

Properly structured trusts established at the right time have repeatedly withstood enforcement attempts. The structuring, the timing, and the post-formation administration matter as much as the choice of jurisdiction.

Contact Us

If you are considering an offshore asset protection trust — or evaluating whether your existing trust is properly structured — contact us at info@dilendorf.com or 212.457.9797 for a confidential consultation.

We assess fit, identify the jurisdiction and structure that match your objectives.