Shopify Suspended Account? Key Tips for Merchants

Online marketplaces such as Shopify have become essential infrastructure for modern commerce. Thousands of merchants rely on these platforms to host storefronts, process payments, and distribute products to customers worldwide.

However, merchants occasionally face sudden disruptions — including account suspensions, frozen payments, or terminated storefronts. When such enforcement actions occur, the merchant’s business can effectively stop overnight.

Understanding the legal framework governing platform relationships is critical for merchants seeking to restore operations and protect their businesses.

Dilendorf Law Firm assists merchants in negotiating disputes with online platforms, including Shopify and other e-commerce marketplaces, and in resolving issues involving suspended stores, frozen payouts, and platform compliance investigations.

Why Shopify May Freeze a Merchant Account

Most online platforms operate under detailed Terms of Service that grant the platform broad authority to enforce compliance with platform rules.

For example, Shopify’s Terms of Service expressly provide that the company may restrict access to its platform:

“Shopify reserves the right to refuse a Merchant access to or use of all or part of the Shop for any reason and at any time without prior notice.”

This contractual authority allows the platform to suspend accounts when it believes a merchant has violated platform policies or applicable law.

Common reasons for Shopify enforcement actions include:

- alleged intellectual property infringement

- counterfeit product complaints

- payment processing or fraud concerns

- regulatory compliance issues

- violations of Shopify’s acceptable use policies

- disputes regarding ownership or control of merchant accounts

Because enforcement systems often rely on automated monitoring or third-party complaints, merchants may find their stores restricted without advance notice.

Platform Terms Limit Shopify’s Role in Merchant Disputes

Another important provision of the Shopify Terms of Service clarifies that the platform does not generally intervene in disputes between merchants and customers:

“As in other areas of the Service, Shopify is not obligated to intervene in any dispute arising between you and your customers.”

This means merchants may be responsible for resolving disputes involving refunds, chargebacks, or product complaints without direct platform assistance.

In addition, Shopify limits responsibility for third-party applications and integrations used by merchants:

“Your use of Third Party Services is entirely at your own risk and discretion.”

The Terms further provide that Shopify may disable access to such services:

“Shopify may disable access to any Third Party Services at any time in its sole discretion and without notice to you.”

Because many merchants rely heavily on third-party applications for payment processing, marketing, or shipping, disabling these services can significantly disrupt operations.

Platform Disputes Can Shut Down Entire Businesses

Modern e-commerce merchants often rely on a single platform to reach customers and process transactions. When platform access is restricted, the impact can be immediate and severe.

Courts have recognized the central role that online marketplaces play in today’s economy. In YCF Trading Inc. v. Skullcandy, Inc., the court described the scale and importance of large online platforms:

“Amazon is the world’s largest online retailer and allows third parties to sell products on its online e-commerce platform, providing third party sellers with exposure to the world marketplace on a scale that no other online retailer can currently provide.”

When marketplace listings are removed or suspended, sellers may lose access to their customers and revenue streams.

Business Disputes Can Lead to Shopify Account Restrictions

Account restrictions may also arise when disputes occur between business partners or competing claimants.

In Browne v. Zaslow, the court described how a Shopify account was created to host an online retail business:

“Beginning his work for the website, J. Browne opened an account with Shopify to serve as the third-party internet host.”

When a dispute arose regarding ownership of the business and its website, Shopify froze access to the account until the parties resolved their disagreement:

“Shopify informed the Parties that it would deny access to the REE account to all concerned until the Parties resolved their differences.”

Such disputes often require legal intervention because the platform may refuse to restore access until ownership issues are resolved.

Federal Consumer Protection Laws Also Affect Online Merchants

Merchants operating through online platforms must comply not only with platform policies but also with federal consumer protection laws.

In FTC v. Romero, the court emphasized that federal law regulates internet-based commerce:

“The Federal Trade Commission Act (FTCA) prohibits unfair or deceptive acts or practices in or affecting commerce.”

Federal regulations governing online orders also impose obligations regarding shipping representations:

“The MITOR prohibits a seller from soliciting any order for the sale of merchandise to be ordered by a buyer via the Internet unless […] the seller has a reasonable basis to expect that it will be able to ship any ordered merchandise.”

Failure to comply with these regulations can trigger enforcement actions from both regulators and platform operators.

Litigation Involving Shopify Platforms

Courts are increasingly addressing legal disputes involving Shopify and similar e-commerce platforms.

In Briskin v. Shopify, Inc., the Ninth Circuit addressed claims arising from Shopify’s role in processing online transactions and collecting user data.

The court explained how Shopify’s technology operates during online purchases:

“When he pressed the ‘Pay now’ button, he had no way of knowing that by doing so he submitted his personal data not to [the merchant], but to Shopify, an e-commerce platform that facilitates online sales for merchants with whom it contracts.”

The court also emphasized that traditional legal principles still apply to internet commerce:

“The emergence of the internet presents new fact patterns, but does not require a wholesale departure from the approach to personal jurisdiction before the internet age.”

These cases demonstrate that courts continue to apply established legal doctrines to modern e-commerce platforms.

Common Legal Issues in Platform Disputes

When merchants face Shopify account suspensions or payment holds, several legal issues frequently arise:

Contract interpretation

Platform relationships are governed by detailed Terms of Service agreements defining platform authority and merchant obligations.

Intellectual property complaints

Brands or competitors may file infringement complaints that trigger listing removal or store suspension.

Ownership disputes

Business partners or investors may dispute control of a merchant account.

Payment processing restrictions

Platforms may freeze payouts during fraud investigations or compliance reviews.

Regulatory compliance

Federal and state consumer protection laws impose obligations on merchants regarding advertising, delivery timelines, and product claims.

What Merchants Should Do If Shopify Freezes Their Store

When Shopify suspends a store or freezes payouts, merchants should take prompt and organized action.

-

Review the suspension notice

Merchants should carefully review any communication received from Shopify, including references to the Terms of Service, Acceptable Use Policy, or Shopify Payments rules.

Identifying the specific issue alleged by Shopify is essential before preparing a response.

-

Preserve business documentation

Merchants should immediately gather records demonstrating compliance with Shopify policies, including:

- supplier invoices

- fulfillment and shipping records

- customer communications

- refund and chargeback history

- intellectual property licenses

These records may be necessary to respond to platform investigations.

-

Respond clearly to Shopify’s investigation

If Shopify allows a response, merchants should provide a structured explanation supported by documentation.

An effective response typically includes:

- explanation of the issue

- supporting evidence

- confirmation of compliance measures

- corrective steps, if applicable

Incomplete responses often delay reinstatement.

-

Address intellectual property complaints

Many Shopify suspensions arise from trademark or copyright complaints.

Merchants should determine:

- who submitted the complaint

- whether the complaint is valid

- whether the products sold are authentic or licensed

Resolving such complaints may require providing proof of authenticity or negotiating with the rights holder.

-

Resolve account ownership disputes

If Shopify freezes an account because multiple parties claim control over it, the platform may refuse to restore access until the dispute is resolved.

Resolving such issues often requires reviewing corporate documents, operating agreements, or partnership agreements.

-

Investigate frozen Shopify Payments payouts

If merchant funds are frozen, Shopify may be investigating:

- chargeback risk

- fraud concerns

- suspicious transaction patterns

- regulatory compliance issues

Merchants should prepare documentation demonstrating legitimate sales and fulfillment activity.

Conclusion

Online marketplaces provide powerful tools for entrepreneurs and retailers, but they also create new legal risks and operational dependencies.

Account suspensions, payment holds, and platform enforcement actions can significantly disrupt a merchant’s business. Courts increasingly recognize the central role these platforms play in modern commerce, yet disputes often turn on the contractual terms governing the platform relationship.

Merchants facing Shopify enforcement actions should evaluate their legal options promptly and seek professional guidance to resolve the dispute efficiently.

Dilendorf Law Firm assists merchants in navigating platform disputes and negotiating with online marketplaces to protect their businesses and restore operations.

Contact Us

If you are facing issues with a suspended Shopify store or restricted merchant account, our firm can review the situation and discuss potential strategies for addressing the dispute.

Whether you are negotiating an ISO agreement, planning to sell a merchant portfolio, or exploring the launch of your own ISO—whether retail or wholesale—legal guidance can help you structure your business, manage risk, and protect your rights.

To schedule a consultation, please contact us at info@dilendorf.com.

Merchant portfolios are often the most valuable asset of an Independent Sales Organization (ISO).

Over time, ISOs develop relationships with merchants that generate recurring revenue through residual payments tied to credit and debit card processing.

Because of the economic value of these portfolios, ISO agreements frequently include Rights of First Refusal (ROFR) that govern how and when a portfolio may be transferred.

Dilendorf Law Firm helps Independent Sales Organizations on negotiating ISO agreements, including provisions governing portfolio transfers and Rights of First Refusal. Careful negotiation of these clauses at the contract stage can significantly affect an ISO’s ability to sell or monetize its merchant portfolio in the future.

Federal and state courts have repeatedly addressed the enforcement of ROFR provisions in commercial contracts and merchant services agreements.

These decisions provide important guidance regarding notice requirements, matching obligations, and the consequences of failing to comply with contractual transfer restrictions.

The Role of ROFR Clauses in ISO Agreements

A Right of First Refusal gives a designated party the opportunity to purchase an asset before it can be sold to a third party. In the merchant services industry, the holder of the right is often the processor or acquiring bank.

Unlike an option contract, a ROFR does not require the owner to sell the asset. Instead, it regulates the circumstances under which a sale may occur.

Courts have described this distinction clearly. In Seessel Holdings v. Fleming Companies, the court explained:

“[…] the right of first refusal, although closely akin to an option, differs in that it does not give the holder the power to compel an unwilling owner to sell, but merely requires that when and if the owner decides to sell, he offers the property first to the holder of the right.”

In the context of ISO agreements, this means that if an ISO receives an offer to sell its merchant portfolio, the processor with ROFR rights must be given the opportunity to match that offer before the portfolio can be transferred.

Enforcement of ROFR Provisions in Merchant Portfolio Transfers

Federal and state cases addressing the enforcement of ROFR clauses in merchant services agreements provide significant guidance on how courts interpret these provisions.

A leading decision is Process America, Inc. v. Cynergy Holdings, LLC, which involved a dispute between an ISO and a processor regarding merchant portfolio transfers. The court described the fundamental structure of the merchant services industry and the role of ISOs:

“Process America is an Independent Sales Organization (“ISO”) that, prior to the termination of their relationship, solicited and referred merchants to Cynergy, a bankcard processor.”

The ISO agreement in that case required compliance with specific contractual conditions before any transfer of merchant accounts could occur. These conditions included providing notice, allowing the processor to exercise a right of first refusal, paying certain fees, and executing a new processing agreement.

When the ISO transferred a portion of the merchant portfolio to a third party without complying with those contractual provisions, the court concluded that the transfer violated the agreement.

The decision underscores a key principle: courts will enforce ROFR provisions in ISO agreements according to their precise contractual language.

When a ROFR Becomes Enforceable

ROFR provisions generally become enforceable when the asset owner receives a legitimate third-party offer.

In Kunelius v. Town of Stow, the First Circuit explained the legal effect of such an offer:

“Once a seller receives a bona fide offer, a right of first refusal (ROFR) ripens into an option to purchase the property at the price and otherwise on the terms stated in the offer.”

The court further emphasized that the holder must have access to the terms of the proposed transaction in order to decide whether to exercise the right.

This principle is particularly important in merchant portfolio transfers because the value of the portfolio may depend on multiple economic terms, including pricing structures, servicing arrangements, and residual payment streams.

The Requirement to Match the Third-Party Offer

Courts consistently require strict adherence to the terms of the third-party offer when exercising a ROFR.

In Seessel Holdings v. Fleming Companies, the court addressed whether the holder had properly exercised its first refusal right and concluded that the holder must accept the same terms offered to the third-party purchaser.

The court explained:

“[…] the right holder who agrees to meet the same terms and conditions as contained in a third-party offer must meet all of those terms.”

The decision further clarified that a party cannot exercise a ROFR while attempting to modify the underlying transaction. If the holder proposes alternative terms or refuses to finalize a contract matching the third-party offer, the attempted exercise of the right may be ineffective.

These principles frequently arise in disputes involving portfolio sales where the processor attempts to match a transaction but proposes different financing structures or contractual conditions.

The Exercise Period and Procedural Requirements

One of the most critical aspects of a ROFR clause is the exercise period and the procedures required to trigger and exercise the right.

There is no statutory default exercise period governing ROFR clauses. The enforceability of the right depends entirely on the contractual language negotiated by the parties.

A properly drafted ISO agreement should clearly define:

- The duration of the exercise period (typically measured in calendar days)

- The triggering event (such as receipt of a bona fide written offer)

- Notice requirements and delivery methods

- Whether failure to respond within the stated period constitutes waiver of the right

If these procedures are not clearly defined, disputes can arise during portfolio sales.

Delayed or Unreasonable Responses by Banks

Problems frequently arise when the processor or acquiring bank fails to respond within the required exercise period or attempts to delay the transaction.

For example, disputes may arise where the bank:

- Responds after the contractual deadline

- Requests additional information not required by the agreement

- Attempts to extend the exercise period unilaterally

- Attempts to renegotiate the transaction instead of matching the offer

Where the agreement clearly defines the exercise period, courts typically enforce the deadline strictly. Failure to exercise the right within that period may result in waiver of the ROFR, allowing the ISO to proceed with the third-party sale.

When the Agreement Does Not Specify an Exercise Period

Additional complications arise when an ISO agreement does not specify the time period for exercising a ROFR.

In such circumstances, courts may determine that the right must be exercised within a reasonable time, based on the surrounding circumstances and commercial expectations of the parties.

However, the absence of a defined deadline creates uncertainty and may delay transactions or discourage potential buyers. For this reason, carefully drafted ISO agreements typically include clear timelines and procedural rules governing ROFR rights.

At Dilendorf Law Firm, we assist ISOs in negotiating and structuring contractual provisions related to Rights of First Refusal in merchant services agreements.

Why ROFR Clauses Matter in Merchant Portfolio Transactions

ROFR provisions are common in ISO agreements because processors and acquiring banks seek to maintain control over the merchant relationships they service.

From a commercial perspective, these provisions help processors:

- Maintain continuity of merchant processing relationships

- Prevent portfolios from being transferred to competing processors

- Protect underwriting and risk management structures

- Preserve long-term merchant revenue streams

For ISOs, however, these provisions may significantly affect exit strategies and portfolio valuation. A buyer negotiating the acquisition of a merchant portfolio must recognize that the transaction could ultimately be acquired by the ROFR holder instead.

Conclusion

Rights of First Refusal play a central role in merchant portfolio transfers within the payment processing industry. Although these provisions do not prohibit portfolio sales, they can significantly influence the outcome of a transaction by determining who ultimately acquires the portfolio and under what conditions.

Courts consistently require strict compliance with ROFR provisions and enforce them according to the language of the governing agreement. For ISOs and processors alike, careful drafting and negotiation of these provisions is essential.

Contact Us

Whether you are negotiating an ISO agreement, planning to sell a merchant portfolio, or exploring the launch of your own ISO—whether retail or wholesale—legal guidance can help you structure your business, manage risk, and protect your rights.

Contact us at info@dilendorf.com to discuss your matter.

In the payment processing industry, merchant portfolios are the core economic asset of an Independent Sales Organization (ISO). They generate residual income, determine exit valuations, and form the foundation of business leverage.

Yet in disputes between ISOs, sub-ISOs, processors, and acquiring banks, one recurring question dominates:

Who actually owns the merchant portfolio?

Federal and state courts consistently provide the same answer:

Ownership, vesting, transfer rights, and residual control are determined by the contract — and courts enforce it strictly.

This article examines how courts analyze merchant portfolio ownership under ISO agreements, focusing on:

- Ownership triggers and vesting

- Transfer restrictions

- Post-termination residual rights

- Conditions precedent

- Survival clauses

- Ambiguity and course of performance

-

Ownership and Vesting: The Contract Controls

The leading appellate decision addressing merchant portfolio ownership is:

Process America, Inc. v. Cynergy Holdings, LLC, 839 F.3d 125 (2d Cir. 2016)

In Process America, the ISO argued that its portfolio ownership vested once it met contractual benchmarks. The agreement defined an “Ownership Trigger Date,” after which ownership would shift.

However, the Second Circuit emphasized that even after the trigger date, the ISO could not freely transfer the merchant agreements. Section 2.6.B imposed strict conditions, including:

- Granting the processor a right of first refusal

- Paying an exit fee

- Executing a new processing agreement acceptable to the processor and bank

The court enforced these conditions as written.

Key takeaway: “Ownership” language in ISO agreements does not necessarily mean unrestricted control. Vesting may be conditional and subject to compliance with multiple contractual prerequisites.

-

Transfer Rights and Restrictions Are Enforceable

In Process America, the ISO solicited merchants and transferred portions of the portfolio without complying with Section 2.6.B. The court found this conduct violated the agreement and caused damages due to merchant attrition.

Courts treat ISO agreements as sophisticated commercial contracts. If the agreement imposes:

- A right of first refusal

- Exit fees

- Consent requirements

- Replacement processing agreements

those restrictions will be enforced.

An ISO cannot circumvent transfer conditions simply because it sourced the merchant relationship.

-

Post-Termination Control and Reserve Funds

Portfolio disputes often arise after termination.

In the related bankruptcy proceeding In re Process America, Inc., 588 B.R. 82 (Bankr. E.D.N.Y. 2018), the court held that the processor was not obligated to release reserve funds until merchant agreements were terminated pursuant to the contract.

Post-termination rights — including reserves and residuals — are governed strictly by the agreement’s language. Courts do not imply broader rights beyond the text.

-

Residual Rights After Termination

Residual income survival is frequently misunderstood.

In Universal Bankcard Systems, Inc. v. Bankcard America, Inc., 998 F. Supp. 961 (N.D. Ill. 1998) the sub-ISO agreement provided that Universal was entitled:

“[…] to receive residuals over the lifetime of its accounts as long as the ISO services the account, […] whether or not this Agreement has been terminated.”

However, the same agreement gave the lead ISO the right:

“[…] sell, at its sole discretion, any portion or all of its merchant base, and in said event, upon the completion of said sale to a bona fide third party, the right of [Universal] to receive residuals arising from said accounts shall cease.”

This dual structure illustrates a critical principle:

Lifetime residual language can be contractually limited by a sale-of-portfolio clause.

Even strong residual survival provisions may be extinguished upon a qualifying sale.

-

The ISO’s Role in Merchant Relationships

Courts also analyze how ISO agreements fit within the broader processing structure.

In Spread Enterprises, Inc. v. First Data Merchant Services Corp., 298 F.R.D. 54 (E.D.N.Y. 2014) the court described the contractual architecture between merchants and processors:

Processors “[…] enter into contracts with different Merchants by which [they agree] to perform several processing functions for the Merchant, such as the authorization, batching, clearing and settlement functions of a credit card transaction.”

Merchant agreements are often:

- Between merchant and acquiring bank

- Sponsored by a processor

- Serviced by an ISO

Thus, an ISO’s “ownership” may refer only to economic rights — not legal ownership of the merchant contract itself.

-

When Do Residual Rights Actually Vest?

Courts distinguish between:

- Accrued rights

- Conditional rights

- Contingent rights

Under federal law, a right is considered vested when it is unconditional and immediately claimable. See Romines v. Great-West Life Assurance Co., 73 F.3d 1457 (8th Cir. 1996).

In the payment processing context, courts routinely examine whether contractual conditions precedent were satisfied before termination.

In Lawson v. Heartland Payment Systems, LLC, 548 F. Supp. 3d 1085 (D. Colo. 2020) the court addressed commission and residual claims in the processing industry employment context.

The court emphasized that compensation rights depend on satisfaction of contractual conditions. If installation, execution, or servicing requirements are not complete at termination, commissions may not vest.

Vesting depends on performance of contractual conditions — not expectations.

-

Conditions Precedent and Contractual Precision

Several courts have refused to recognize vesting where required steps were not completed.

If an ISO agreement ties residual rights to:

- Executed merchant contracts

- Approved applications

- Installed terminals

- Active servicing

then those elements must be satisfied before vesting occurs.

Absent fulfillment of conditions precedent, residual claims may fail.

-

Ambiguity and Course of Performance

When contractual language is ambiguous, courts may examine extrinsic evidence.

For example, in Orkin v. Albert, 162 F.4th 1 (2025), the court relied on the parties’ conduct — including forwarding of residual payments — to interpret ownership intent.

However, where the language is clear, courts will enforce the agreement as written, even if the result appears harsh.

Conclusion: Portfolio Ownership Is a Contractual Allocation of Risk

The consistent judicial theme across Process America, Universal Bankcard, Spread Enterprises, and related decisions is unmistakable:

Ownership, vesting, transfer rights, and residual survival depend entirely on the contractual structure.

An ISO may believe it “owns” its portfolio. But unless the contract supports that belief — and all conditions are satisfied — courts will enforce the agreement as written.

Merchant portfolio disputes are not emotional disputes about business relationships.

They are contractual disputes governed by precise drafting.

Contact Us

Whether you are negotiating an ISO agreement, planning to sell a merchant portfolio, or exploring the launch of your own ISO—whether retail or wholesale—legal guidance can help you structure your business, manage risk, and protect your rights.

Contact Dilendorf Law Firm at info@dilendorf.com to schedule a confidential consultation.

If you sent crypto on the wrong network to a U.S. exchange, Dilendorf Law Firm can help. The firm focuses on crypto disputes and arbitration for U.S. customers.

How U.S. exchanges treat wrong‑network deposits

U.S. exchanges try to put all “wrong network” risk on you. Their user agreements and help pages say that unsupported or mis‑sent deposits are your problem, not theirs.

Support teams quote this language when they tell you your funds are “lost” or “irrecoverable.”

Coinbase (U.S.): “not liable” for unsupported assets

Coinbase’s U.S. User Agreement warns that you may use your wallet only for “Supported Digital Assets.”

-

“Your Digital Asset Wallet is intended solely for proper use of Supported Digital Assets as designated on the Coinbase Site.”

-

“Under no circumstances should you attempt to use your Digital Asset Wallet to store, send, request, or receive any assets other than Supported Digital Assets. Coinbase assumes no responsibility in connection with any attempt to use your Digital Asset Wallet with Digital Assets that we do not support.”

-

“You acknowledge and agree that Coinbase is not liable for any unsupported Digital Asset that is sent to a wallet associated with your Coinbase Account.”

If you send crypto over an unsupported network, Coinbase points to this language. It tells users that such assets “may be permanently lost” and that it “cannot recover these assets or funds.”

Coinbase sometimes offers “asset recovery” tools. But those are discretionary. The contract is written so Coinbase can say it does not owe you a duty to recover.

Binance.US: “unable to recover/return” unsupported deposits

Binance.US uses similar wording. Its help center is blunt about wrong‑network deposits.

-

“Binance.US is unable to recover/return deposits of unsupported assets or deposits sent using unsupported networks.”

-

It notes that sending to the wrong network “often lead[s] to irrecoverable funds.”

-

Another page adds: “Binance.US is not liable for any losses if you deposit an unsupported asset, deposit assets using an unsupported network, or transfer an asset to an address not owned by Binance.US.”

Binance.US has a “Deposit Recovery Tool” for some cases. But it excludes unsupported assets and unsupported networks.

Uphold: refusing to retrieve funds on unsupported networks

Uphold takes the same position. In complaints involving wrong‑network transfers, Uphold admits the funds are at a wallet linked to your account but still refuses to act.

In one BBB response, Uphold wrote:

-

“Although the transaction appears on the blockchain at an address associated with your Uphold account, our platform infrastructure does not support access to assets on unsupported networks.”

-

“While we sympathize with the situation and understand that mistakes can happen, we regret to inform you that we are unable to retrieve or return funds sent via unsupported networks at this time.”

Users report the same outcome. If the asset or network is “unsupported,” Uphold tells them: “we cannot recover them. They’re gone!”

What this means for U.S. victims

The pattern is clear:

-

Exchanges define what is “supported.” They can change this at any time.

-

If you send crypto on an unsupported network, they say they are “not liable” and “unable to recover/return” your funds.

-

They use this language to close your ticket, even when blockchain data shows the funds in an exchange‑controlled wallet.

Many victims stop there. They assume there are no options.

How Dilendorf Law Firm helps

Max Dilendorf and Dilendorf Law Firm focus on exactly these kinds of disputes. The firm has handled more than 130 cybercrime and crypto‑related arbitrations against exchanges and telecom carriers in U.S. forums such as AAA, JAMS, and NAM.

Here is how the firm approaches wrong‑network cases:

-

Read the contract. The team analyzes the U.S. user agreement, risk disclosures, and arbitration clause that applied to your account and date of loss.

-

Trace the funds. Using blockchain tools, they show your funds reached an address controlled by the exchange.

-

Attack one‑sided terms. In arbitration, they argue that boilerplate “not liable” language cannot excuse an exchange when its own design, warnings, or support behavior helped cause the loss.

-

Run the arbitration. They draft the demand, handle discovery, work with experts, and present your case at the hearing. They have already done this in 130+ cyber and crypto matters.

This is core work for the firm, not a side project.

When to contact Dilendorf Law Firm

Consider contacting Dilendorf Law Firm if:

-

You are a U.S. customer.

-

You sent BTC, ETH, USDT, USDC, or another asset to Coinbase, Binance.US, Uphold, or another U.S. platform on the wrong network.

-

Support pointed you to language like “not liable for any unsupported Digital Asset” or “unable to recover/return deposits of unsupported assets or deposits sent using unsupported networks.”

The firm can review your transaction, explain the terms that exchanges rely on, and outline arbitration or other strategies.

With experience in more than 130 crypto and cybercrime arbitrations, Dilendorf Law Firm is well‑positioned to challenge “lost forever” responses and pursue recovery of wrong‑network deposits

Venue provisions in an ISO agreement are not secondary terms. They determine where and how disputes over residual payouts, portfolio ownership, termination, rights of first refusal, or indemnification will be resolved.

The choice between federal court, state court, and arbitration can materially affect cost, timing, leverage, and outcome.

For ISOs, venue is a strategic business decision—not merely a procedural clause.

Arbitration: The Dominant ISO Model

Most modern ISO agreements require mandatory arbitration, typically administered by:

- AAA (American Arbitration Association)

- JAMS

- NAM (National Arbitration and Mediation)

Arbitration clauses are strongly favored under the Federal Arbitration Act (FAA).

In Henry Schein, Inc. v. Archer & White Sales, Inc., 586 U.S. 63 (2019), the Supreme Court made clear:

“Under the Federal Arbitration Act (FAA), arbitration is a matter of contract, and courts must enforce arbitration contracts according to their terms.”

The Court further emphasized:

“The Federal Arbitration Act does not contain a ‘wholly groundless’ exception, and courts are not at liberty to rewrite the statute passed by Congress and signed by the President.”

Similarly, in AT&T Mobility LLC v. Concepcion, 563 U.S. 333 (2011), the Court reinforced the federal policy favoring arbitration and the principle that arbitration agreements must be enforced as written.

The practical takeaway for ISOs is straightforward: arbitration clauses—including venue designations, delegation provisions, and class-action waivers—are rarely invalidated.

Venue Under the FAA

The FAA also governs arbitration-related venue mechanics.

In Cortez Byrd Chips v. Bill Harbert Constr. Co., 529 U.S. 193 (2000), the Supreme Court held that the FAA’s venue provisions in §§ 9–11 are permissive rather than restrictive, meaning courts may confirm or vacate arbitration awards in more than one permissible venue.

However, compelling arbitration under 9 U.S.C. § 4 is treated differently. Federal courts have recognized that § 4 contains mandatory language requiring arbitration to proceed within the district where the petition to compel is filed.

These distinctions matter when drafting arbitration and venue language in ISO agreements.

Federal and State Court Litigation

If an ISO agreement designates litigation rather than arbitration, forum-selection clauses are also strongly enforced.

In The Bremen v. Zapata Off-Shore Co., 407 U.S. 1 (1972), the Supreme Court held:

“Forum-selection clauses are prima facie valid and should be enforced unless enforcement is shown by the resisting party to be unreasonable under the circumstances.”

The Court further explained:

“Where the choice of a forum was made in an arm’s-length negotiation by experienced and sophisticated businessmen, absent some compelling and countervailing reason, it should be honored by the parties and enforced by the courts.”

In other words, once a venue clause is agreed upon, courts will rarely disturb it.

Why ISOs Often Choose Arbitration

ISOs frequently accept arbitration because it offers:

- Faster resolution

- Confidential proceedings

- Streamlined procedures

- Decision-makers with commercial expertise

Confidentiality alone can be critical in disputes involving residual streams, merchant portfolios, or termination rights.

The Cost Reality

Arbitration is often faster—but not necessarily cheaper.

Unlike courts, arbitration requires:

- Administrative filing fees

- Arbitrator hourly compensation

- Institutional fees (AAA, JAMS, NAM)

- Hearing logistics and scheduling costs

In complex ISO disputes—particularly those involving forensic accounting, portfolio valuation, or multi-year residual calculations—arbitration costs can exceed federal court litigation.

Additionally, arbitration awards are subject to extremely limited judicial review. Errors of law are rarely grounds for reversal.

Arbitration and Venue: Strategic Review Before Signing

An arbitration clause should be reviewed carefully before signing an ISO agreement. ISOs should confirm:

- Which organization will administer the arbitration (AAA, JAMS, or NAM);

- Where the arbitration will take place;

- Whether the case will be decided by a single arbitrator or a panel;

- How arbitration fees and attorneys’ fees are allocated;

- How broadly the clause is drafted;

- Whether any claims are carved out for court relief.

Language covering disputes “arising out of or relating to” the agreement may capture nearly all claims, including termination, indemnification, rights of first refusal, liability caps, and residual calculations.

Because courts “must enforce arbitration contracts according to their terms,” and forum-selection clauses are “prima facie valid,” venue provisions are rarely negotiable after a dispute arises.

A mandatory arbitration clause combined with fee-shifting may increase financial exposure. Conversely, a carefully negotiated clause can preserve leverage in a dispute with a payment processor or sponsoring bank.

Venue is not merely procedural—it is strategic.

Protect Your Position Before You Sign

At Dilendorf Law Firm, we represent ISOs and payment industry participants in negotiating ISO agreements, including arbitration clauses, venue provisions, residual payout protections, rights of first refusal, and risk allocation mechanisms.

Whether you are negotiating an ISO agreement, planning to sell a merchant portfolio, or exploring the launch of your own ISO—whether retail or wholesale—legal guidance can help you structure your business, manage risk, and protect your rights.

Contact us at info@dilendorf.com to protect your residual income, portfolio rights, and strategic position.

When a victim’s phone is stolen and cryptocurrency is drained from an exchange account, exchanges and telecommunications carriers often argue that the loss was caused solely by third-party criminals.

Dilendorf Law Firm represents victims whose phones were stolen and thieves initiated unauthorized activity from the victims’ cryptocurrency exchange accounts.

The firm handles disputes involving account takeovers, SIM-swap attacks, and rapid unauthorized withdrawals.

Courts do not automatically accept the “third-party criminal” defense.

Courts examine if an exchange’s own security systems, authentication controls, monitoring procedures, or response measures contributed to the loss.

These cases are highly fact-intensive and high risk. Most exchanges require arbitration.

They assert broad contractual defenses.

Duty to Implement Adequate Security Measures

In Yuille v Uphold HQ Inc., 686 F Supp 3d 323, 335-336 (S.D.N.Y. 2023), the court summarized allegations that the exchange failed to safeguard customer accounts. The complaint alleged that Uphold failed to provide adequate security by:

“failing to provide reasonable and appropriate security to prevent unauthorized access to its customer’s account … misrepresenting ‘the safety and security of’ its accounts … failing ‘to adequately safeguard and protect’ the accounts; [and] failing ‘to use readily available security measures to prevent or limit unauthorized access to customer accounts and to prevent unauthorized transactions from occurring on those accounts.’”

The case reflects that exchanges may face liability where internal controls are insufficient to prevent foreseeable unauthorized access.

In Rider v Uphold HQ Inc., 657 F Supp 3d 491, 496 (S.D.N.Y. 2023), the plaintiffs challenged the exchange’s authentication architecture.

The court described allegations that Uphold’s implementation of two-factor authentication allowed unauthorized users to access accounts without the original device, thereby compromising account security.

In a stolen-phone case, these allegations are critical.

If authentication can be bypassed without meaningful device verification, biometric confirmation, or withdrawal delays, plaintiffs could argue that the exchange’s security design contributed to the loss.

Negligence and Weakened Safeguards

In Yuille, the court also described allegations that user-experience changes weakened security protections.

The complaint alleged that measures adopted to improve customer service:

“weakened its account security by reducing the situations in which Uphold would restrict [unauthorized] account access.”

Negligence claims often focus on operational failures.

These may include failing to suspend credentials after repeated failed login attempts, failing to delay withdrawals after password resets, or failing to flag large transfers to newly added wallets.

If safeguards are relaxed for convenience, plaintiffs may argue that reasonable care was not exercised.

Misrepresentation of Security Standards

Exchanges frequently advertise strong protections. In Pillar Project AG v Payward Ventures, Inc., 64 Cal App 5th 671, 674, 279 Cal Rptr 3d 117, 121 (2021), the court described allegations that the exchange:

“…falsely advertised that it provided the best security in the business.”

and that those measures were

“...failed to use standard security measures on its exchange which would have prevented the theft.”

If an exchange promotes “bank-level security” or “advanced fraud monitoring,” yet fails to stop rapid unauthorized withdrawals after a phone theft or SIM-swap attack, those statements may support misrepresentation claims.

Role of Telecommunications Carriers

Stolen-phone and SIM-swap cases often involve telecommunications carriers.

Major carriers such as Verizon, AT&T, and T-Mobile may be implicated where unauthorized SIM swaps or account changes enabled access to exchange accounts.

If a carrier transfers a number without proper identity verification, disables PIN protections, or fails to detect suspicious account activity, plaintiffs may assert negligence or statutory claims against the carrier.

Liability analysis often requires examining both the exchange’s authentication systems and the carrier’s account-security procedures.

Arbitration and High-Risk Litigation

These cases are high risk. Major exchanges, including Coinbase, Binance, Gemini, and Uphold, require arbitration.

They assert assumption-of-risk defenses and argue that possession of login credentials constitutes authorization.

They also argue that third-party criminal acts break the chain of causation.

Carriers raise contractual limitations and federal preemption defenses. Success depends on forensic evidence.

This includes IP logs, device fingerprints, authentication records, internal security policies, SIM-swap documentation, and timing of notice.

Dilendorf Law Firm’s Experience

Dilendorf Law Firm represents victims in stolen-phone and SIM-swap cases involving unauthorized cryptocurrency transfers.

The firm represents clients in disputes against Coinbase, Binance, Gemini, Uphold, and other exchanges.

The firm also represents clients in cases against Verizon, AT&T, T-Mobile, and other telecommunications carriers.

To date, the firm has arbitrated more than 130 cases against crypto exchanges and phone carriers.

These matters involve complex arbitration clauses, evolving regulatory standards, and sophisticated technical evidence.

Stolen-phone cryptocurrency disputes are not routine consumer claims.

They are high-risk, high-stakes proceedings that require experienced arbitration counsel and detailed forensic investigation.

Conclusion

Cases such as Yuille, Rider, Pillar Project, and Widjaja show that exchanges and financial institutions are not automatically insulated from responsibility when unauthorized transfers follow a phone theft.

Plaintiffs may establish liability by demonstrating inadequate safeguards, weakened controls, misleading security representations, or failure to act promptly after notice. Carrier conduct may also be central to the analysis.

At the same time, these cases are complex, arbitration-driven, and high risk.

Careful evaluation of contracts, regulatory obligations, and technical evidence is essential before proceeding.

Contact Us

If your phone was stolen and thieves transferred cryptocurrency or funds out of your exchange account without your authorization, contact Max Dilendorf at Dilendorf Law Firm.

Email: max@dilendorf.com

Phone: 212.457.9797

Early action is critical in stolen-phone and unauthorized crypto transfer cases. Prompt investigation can help preserve evidence and assess potential claims against exchanges and telecommunications carriers.

SIM Swap Attacks in 2026: What Victims Need to Know

If you believe you were the victim of a SIM swap attack and lost cryptocurrency or access to your accounts, start with the video above. It explains what likely happened and what legal options may be available.

SIM swap attacks are rapidly increasing in 2026. They are now one of the most damaging forms of cybercrime affecting crypto holders, investors, and everyday consumers.

These attacks often begin when a mobile carrier transfers a customer’s phone number to a SIM card controlled by a criminal.

Once that happens, the attacker receives your calls, text messages, and security codes.

They can reset passwords and access email accounts, crypto exchanges, and self-custody wallets. In many cases, cryptocurrency and other assets are stolen within minutes.

Victims often realize what happened only after their phone stops working.

Many people searching for a SIM swap attorney or SIM swap lawyer are surprised to learn how complex these cases can be.

SIM swap attacks frequently involve failures by wireless carriers such as T-Mobile, Verizon, AT&T, or other providers.

These failures may include weak authentication procedures, ignored security flags, or unauthorized SIM transfers.

When carrier security failures lead to stolen cryptocurrency or financial losses, victims may have legal claims.

These claims are often pursued through arbitration or litigation under federal telecommunications law and consumer protection rules. Timing matters. Evidence can disappear quickly, and deadlines may apply.

In the video above, Max Dilendorf, founder of Dilendorf Law Firm, explains how SIM swap attacks work.

He also discusses why these crimes are accelerating in 2026 and what victims should do immediately after discovering an attack.

Dilendorf Law Firm has handled more than 130 cybercrime and crypto-related matters. These include SIM swap attacks, cryptocurrency theft, software liability disputes, and AI-related fraud.

The firm regularly represents victims in complex arbitration cases against major mobile carriers.

This video is designed to help victims understand their rights. It explains why acting quickly is critical. It also outlines how working with an experienced SIM swap lawyer can help victims evaluate potential recovery options.

Resources:

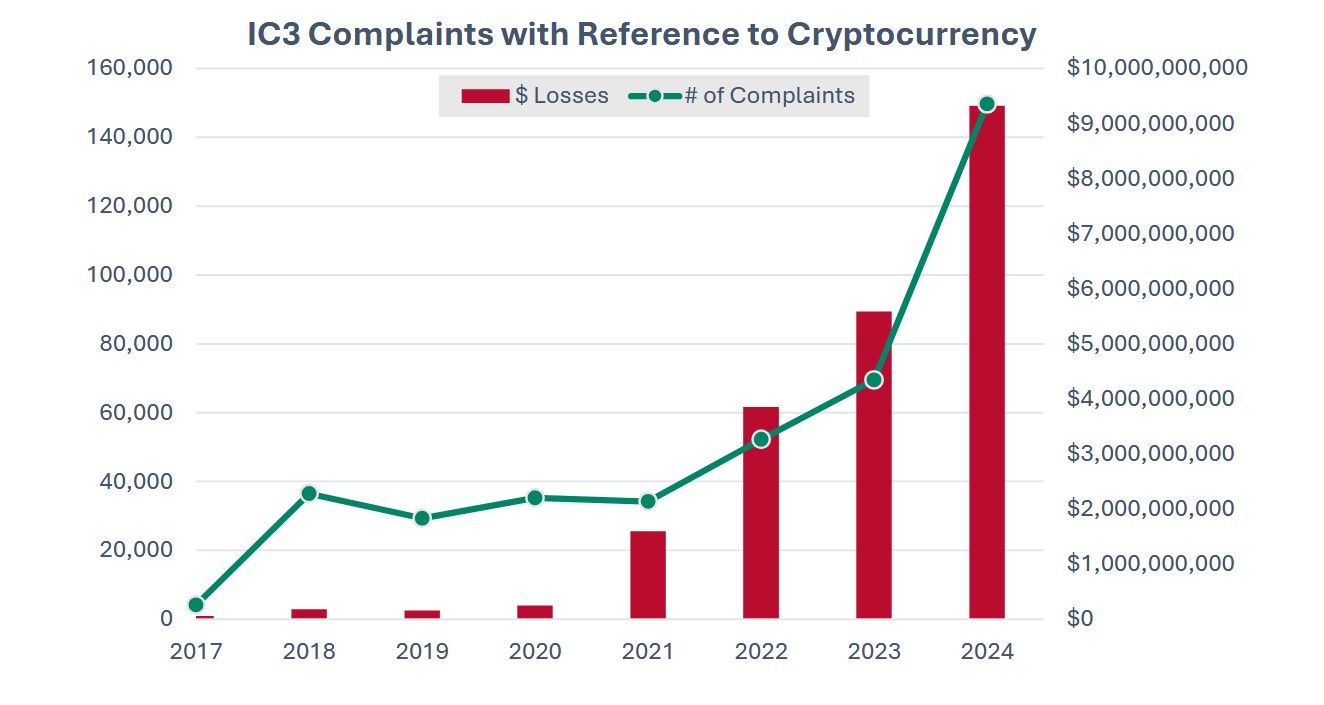

- Cryptocurrency – Internet Crime Complaint Center (IC3)

- NYDF Consumer Complaint

- AAA Consumer Arbitration Rules

- JAMS Comprehensive Arbitration Rules & Procedures

- Crypto Enforcement

- Modern Scams: How Scammers are Using Artificial Intelligence and How We Can Fight Back

- Cryptocurrency Fraud Report 2023

- Cryptocurrency: Selected Policy Issues

- Combatting Illicit Activity Utilizing Financial Technologies and Cryptocurrencies

- Crypto-Assets: Implications for Consumers, Investors, and Businesses

- Exploring the Cryptocurrency and Blockchain Ecosystem

- Crypto Assets

- What To Know About Cryptocurrency and Scams

- Digital Assets | CFTC

- Taxpayers need to report crypto, other digital asset transactions on their tax return

Crypto Stolen from Coinbase or Another Exchange? Dilendorf Law Can Help

If your cryptocurrency was stolen from Coinbase or another U.S.-based crypto exchange and the platform denied responsibility, you may still have legal options.

Many victims are told there is nothing an exchange can do—but that is often not the end of the story.

In this video, Max Dilendorf, a New York–based crypto attorney, explains how exchange User Agreements and mandatory arbitration clauses can provide a legal path forward for recovering stolen crypto.

👉 Watch the full video on YouTube:

What This Video Is About

This video focuses on one of the most misunderstood—but most important—documents in crypto disputes: the User Agreement you accepted when opening your exchange account.

Since 2017, Dilendorf Law has worked exclusively in the crypto space.

Since 2019, the firm has been among the first in the U.S. to represent victims of exchange-related crypto theft in arbitration and litigation. To date, the firm has handled 130+ arbitration cases involving stolen customer funds.

In this episode, Max explains:

-

Why exchanges rely on User Agreements to deny liability

-

How arbitration clauses often replace lawsuits as the only legal remedy

-

Why these agreements are legally enforceable—even if you never read them

-

How missing a notice or procedural step can permanently block your claim

Key Topics Covered in the Video

1. Reviewing the Exchange User Agreement

If an exchange refuses to reimburse stolen funds, the User Agreement becomes the legal roadmap for your claim. Max explains how to locate and analyze the dispute resolution and arbitration sections.

2. Understanding Mandatory Arbitration

Most U.S. crypto exchanges require disputes to be resolved through private arbitration—not court. The video explains how arbitration works, why it is binding, and what limitations apply.

3. Notice Requirements Before Arbitration

Many exchanges require victims to send a formal written notice before filing arbitration. The video explains common deadlines (30–60 days), delivery methods, and why failing to comply can derail a case.

4. Choosing the Arbitration Forum

The video breaks down the most common arbitration providers used by crypto exchanges:

-

American Arbitration Association (AAA)

-

JAMS

-

National Arbitration and Mediation (NAM)

Each forum has different rules, fees, and procedures—experience matters.

5. Why Legal Strategy Matters

Arbitration decisions are usually final, with limited appeal rights. Max explains why preparation, proper filing, and legal strategy significantly affect outcomes in stolen-crypto cases.

Who Should Watch This Video

This video is especially relevant if:

-

Your Coinbase or exchange account was hacked

-

You experienced unauthorized withdrawals or transfers

-

The exchange denied reimbursement or blamed the user

-

You’re unsure how arbitration works or where to start

Need Legal Help After Crypto Theft?

If your crypto was stolen and the exchange refused to help, you may still have options—but timing and procedure are critical.

Contact Dilendorf Law:

📧 info@dilendorf.com

📞 212-457-9797

This video is for educational purposes only and does not constitute legal advice. For guidance specific to your situation, consult a qualified crypto attorney.

U.S. & International Asset Protection and Estate Planning for High-Risk Professionals and Global Entrepreneurs

In this video, Max Dilendorf, founder of Dilendorf Law Firm, explains how individuals and business owners can protect assets in an increasingly aggressive legal and regulatory environment through sophisticated U.S. and international planning strategies.

Dilendorf Law Firm represents U.S. and non-U.S. clients worldwide, including doctors, surgeons, physicians, entrepreneurs, real estate developers, architects, and other high-risk professionals who require advanced asset protection and long-term wealth preservation.

We also advise international clients moving businesses or investments to the United States, providing cross-border tax planning, tax structuring, and U.S. business formation services.

The video discusses both onshore and offshore asset protection solutions, including:

-

U.S. asset protection trusts and dynasty trusts in favorable jurisdictions such as Alaska, Wyoming, Delaware, and South Dakota

-

Offshore trust and holding structures in jurisdictions including the Cayman Islands, Cook Islands, Switzerland, Liechtenstein, Nevis, and the United Arab Emirates

-

Integrated estate planning for families with U.S. and international assets

-

Compliant planning for U.S. and foreign real estate ownership

Max also addresses the firm’s extensive experience in crypto law and digital asset protection, including secure custody strategies and crypto-related litigation, and how digital assets can be incorporated into a broader asset protection and estate planning framework.

Whether you are a U.S. professional seeking protection from litigation risk, or an international business owner navigating U.S. tax and compliance rules, this video outlines how a carefully structured, fully compliant global “Plan B” can help safeguard wealth across borders.

Contact Us

If you are considering U.S. or international asset protection, estate planning, or cross-border business structuring, contact Dilendorf Law Firm for a confidential consultation.

Email: info@dilendorf.com | Phone: 212.457.9797

Our team works with clients in the United States and internationally to develop compliant, strategic solutions tailored to complex risk profiles and global assets.

On December 17, 2025, Coinbase introduced an updated version of its User Agreement.

While many users expected major changes to arbitration and dispute‑resolution rules, those provisions were not amended and continue to govern how hacked‑account and stolen‑funds disputes must be resolved in 2026.

For victims whose crypto was stolen from Coinbase, understanding how these terms allocate risk, limit liability, and channel claims into arbitration is critical to planning an effective recovery strategy.

New Services, Same Arbitration Framework

The update primarily adds and clarifies new services rather than changing the core dispute‑resolution mechanics.

-

Coinbase introduced a Token Sale Platform that lets users purchase newly issued digital assets directly from third‑party developers, with Coinbase acting only as a platform provider.

-

The agreement clarifies that U.S. equities trading is conducted through Coinbase Capital Markets Corporation, a registered broker‑dealer affiliate that is legally separate from Coinbase’s digital asset services.

Even with these additions, the mandatory arbitration provisions and class‑action waiver that apply to most crypto‑related disputes remain in place.

Limitation of Liability

The User Agreement continues to impose significant limitations on Coinbase’s liability.

In most circumstances, a user’s potential recovery is capped at the value of the supported digital assets held in the user’s wallet at the time the claim arises.

Users also generally waive the right to recover lost profits, loss of business opportunities, diminution in value, data loss, or other indirect or consequential damages.

Coinbase also provides its services on an “as is” and “as available” basis, disclaims most warranties, and does not guarantee that transactions will be executed accurately or at all.

Liability beyond these limits is permitted only if a court makes a final determination that the harm resulted from Coinbase’s gross negligence, fraud, willful misconduct, or intentional violation of law.

Coinbase’s allocation of responsibility for account security remains unchanged. The User Agreement places responsibility on users for safeguarding login credentials and expressly disclaims liability for losses resulting from compromised credentials, unauthorized access, or misuse of the Trusted Contacts feature.

Coinbase’s Formal Complaint Process remains unchanged

The User Agreement’s Formal Complaint Process remains unchanged.

Under Section 7.2, users must first attempt to resolve any dispute by contacting Coinbase Support.

If the dispute is not resolved through Coinbase Support, users are required to complete Coinbase’s Formal Complaint Process before filing any arbitration claim under Section 7.3.

Failure to complete the Formal Complaint Process may result in dismissal of the arbitration.

If a dispute proceeds to the Formal Complaint Process, users must submit a complaint using Coinbase’s designated complaint form (or request the form from Coinbase Support), describing the dispute, the requested resolution, and any relevant information.

The Formal Complaint Process is deemed complete when Coinbase responds to the complaint or forty-five (45) business days after Coinbase receives it, whichever occurs first.

Because arbitration cannot be initiated until this process is completed, the Formal Complaint Process serves as a mandatory procedural prerequisite to arbitration under the User Agreement.

For a step-by-step overview of how to comply with Coinbase’s Formal Complaint Process, see:

Arbitration Process Remains Unchanged

The User Agreement’s arbitration provisions also remain unchanged.

Once the Formal Complaint Process is completed, disputes that are not resolved must continue to be pursued through binding arbitration in accordance with the procedures set forth in the User Agreement.

For a detailed, step-by-step overview of how Coinbase arbitration works in practice – including filing requirements, timelines, and procedural considerations – see our previously published guide:

Users should also be aware that the User Agreement continues to include a broad waiver of procedural rights.

Claims against Coinbase must be brought on an individual basis only, and users waive the right to participate in class, collective, or representative actions.

In addition, the User Agreement expressly includes a jury trial waiver, meaning that if any dispute were to proceed in court, it would be resolved by a judge rather than a jury.

The arbitration provisions further permit fee-shifting in limited circumstances. A user may be required to pay Coinbase’s attorneys’ fees and costs if an arbitrator determines that a claim was frivolous or brought for an improper purpose, or if a court finds that the user failed to satisfy required pre-arbitration conditions.

Contact Us

If your Coinbase account was hacked and your crypto was stolen, contact Dilendorf Law Firm to discuss your recovery options and case strategy.

Our team has represented victims in 130+ crypto cyber-theft arbitrations across major forums (AAA, JAMS, NAM), including cases against Coinbase and other leading U.S. exchanges.

The firm focuses on stolen-crypto recovery, SIM-swap and account-takeover cases, and User Agreement–based arbitration claims, integrating blockchain forensics and coordinated law-enforcement engagement where appropriate.

Led by crypto attorney Max Dilendorf (practicing in this space since 2017), the firm represents clients nationwide and internationally in high-stakes exchange disputes.

Email info@dilendorf.com or call (212) 457-9797 to schedule a confidential consultation about your Coinbase theft case.