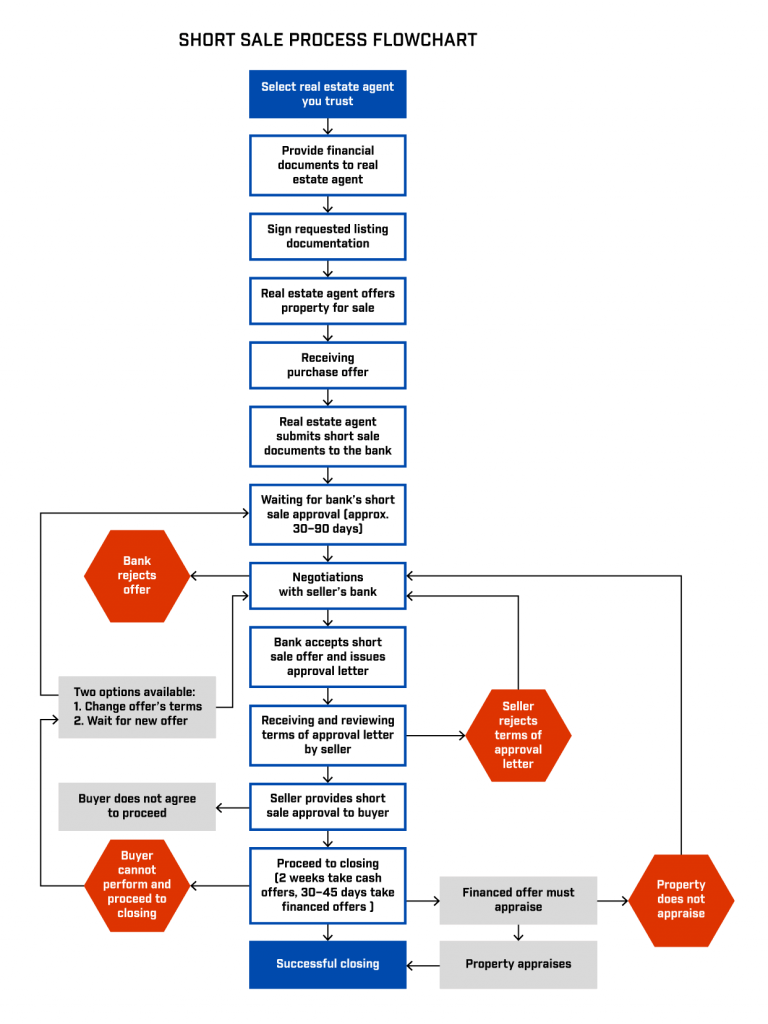

When you can go into short sale?

Usually short sale is acceptable when the homeowner realizes that he can no longer afford mortgage payments. Instead of waiting for the bank to foreclose, the homeowner initiates the short sale process by submitting an application to the lender.

There are two critical factors that the lender will consider when deciding whether to approve a short sale:

- The real estate has to be worth less than what the owner owes on it. The lender will want to review recent sales of comparable properties to make sure of this.

- The seller must be able to prove financial hardship. The lender may ask to show that owner doesn’t have the income or assets to pay back the rest of the outstanding

What Are the Benefits of a Short Sale?

A short sale is more beneficial and less damaging to seller as it gives possibility to avoid the negative impact of a foreclosure. In general, after a foreclosure sellers are required to wait seven years before obtaining another mortgage loan, while a short sale may cause you to wait two years. Also short sale releases you from the mortgage obligations on the property.

A short sale also beneficial to buyer, as it helps to buy at bargain price valuable real estate.

As seller pays off only part of the debt, the lender takes a financial loss, however it is less damaging as it could be after foreclosure.

What are the risks of a Short Sale?

Common issues in short sale transactions:

- A seller may be required to sign a promissory note for the amount of any deficiency or the lender may not “forgive” the deficiency and pursue the seller for that amount at a later date. In either case, the seller still owes the money, but the lender’s security interest in the property is simply released so the property can be sold.

- If there are multiple lenders or lien holders (such as a 2nd or 3rd position lenders) the holders of the subordinate liens may seek a deficiency judgment against the seller.

- Any forgiven debt may be considered taxable income for Federal Income purposes.

- A sale made to avoid foreclosure could be considered a “Fraudulent Conveyance” if not made for a reasonable price.

- Some mortgage contracts contain a “due on sale” clause. This is particularly important when there is “cross collateralization.” A delinquency on, or a sale of, one property owned by a borrower can trigger a due on sale clause on another property

Lender Approval Process

When a lender approves a short sale and receives a “short payoff,” that approval is often conditioned on certain requirements and the seller may be required to sign affidavits or other documents verifying these requirements are met.

Some common conditions include the following:

- The seller cannot receive any proceeds from the sale including a sales commission, a negotiator’s fee, or any sum that is not disclosed to the lender.

- The sale does not involve a “flip” transaction. Thus, it is important that brokers disclose all terms of the transaction.

- The property is marketed at a fair price. Short sale properties may not be listed for an amount greater than the fair market value to discourage buyers from presenting an offer or for far less than their fair market value to convince the lender that the property will not sell for a higher amount. A broker owes a duty to deal honestly and in good faith with all parties to a transaction. In addition, a broker may not knowingly commit, or be a party to, any material fraud, misrepresentation, trick, or scheme, whereby any other person lawfully relies upon the word, representation or conduct of the broker. Brokers that deceive or aid in the deception of a lender are subject to enforcement action.

What we offer?

We offer legal support that covers all phases of short sale, in particular negotiations between the parties, drafting and proofreading of all short sale documents, resolving any pre-closing issues, client’s representation at closing.

Options Other Than Short Sale

A short sale may not be your best course of action. Consider all your options before making a decision.

Loan Workout

- Reinstatement: Paying the total amount owed by a specific date in exchange for the lender agreeing not to foreclose.

- Forbearance: An agreement to reduce or suspend payments for a short period of time.

- Repayment Plan: An agreement to resume making monthly payments with a portion of the past due payments each month until they are caught up.

- Claim Advance/Partial Claim: If the loan is insured, a homeowner may qualify for an interest-free loan from the mortgage guarantor to bring the account current.

Loan Modification

- The lender may agree to change the terms of the original loan to make the payments more affordable. For example, missed payments can be added to the existing loan balance, the interest rate may be modified or the loan term extended. Lenders may use government program modifications or may use their own criteria. Loan modifications may be temporary or permanent. Loan modification resources include:

Resources:

Please note the information provided does not, and is not intended to, constitute legal advice. Instead, the information is for general informational purposes only.

Dilendorf, Esq.")