At Dilendorf Law Firm, we are dedicated to empowering New York residents with comprehensive asset protection and estate planning solutions.

Our skilled attorneys specialize in crafting both foreign and domestic asset protection trusts, tailored to the unique needs of each client.

New Yorkers face distinctive challenges in asset protection due to the absence of a state-specific domestic asset protection statute. This lack can leave assets more exposed to legal disputes and creditor claims.

ATTORNEYS' EXPERIENCE

ATTORNEYS' EXPERIENCE

Dilendorf Law Firm represents U.S. and international clients in complex estate and asset protection matters, including domestic asset protection trusts (DAPTs) and offshore trust structures in leading jurisdictions worldwide.

Domestic Asset Protection Laws – Are They Effective for NY Residents?

Nationally, 19 states have enacted Domestic Asset Protection Trusts (DAPT) laws, providing significant safeguards for their residents’ assets. Yet, New Yorkers establishing a DAPT in another state might encounter legal hurdles. Creditors could potentially challenge the trust’s validity, exploiting the lack of a corresponding New York statute.

Our experience with New York’s business owners, entrepreneurs, and real estate professionals has shown a preference for using DAPT structures for asset and estate planning.

In our professional experience, we frequently observe New York business owners, entrepreneurs, real estate professionals opting for DAPT asset and estate planning trusts. Nonetheless, it’s crucial to recognize that the fundamental principle of “full faith and credit” requires that each state within the U.S. must recognize and respect judgments from sister states.

It’s essential to note that 31 states, including New York, Florida, Texas, and California, lack DAPT statutes.

In situations where, for example, a business owner becomes entangled in a contract dispute or tort case in New York while holding a DAPT trust in a state such as Wyoming or Nevada, creditors may have strong grounds to assert claims against the developer’s assets located within a DAPT trust.

Enforcing an out-of-state judgment typically involves a “conflict of law” analysis in the enforcing state, often a DAPT state. Notably, the new Section 10 of the Uniform Voidable Transactions Act (already adopted by 20 states) stipulates that it is the debtor’s home state law that applies, not the DAPT jurisdiction.

In the case of a DAPT state, if the only connection to that state is the existence of a trust where you are both the beneficiary and grantor, the judge may look beyond the trust’s physical location. In deciding the enforceability of the judgment, the judge is likely to apply the law of the state where the tort occurred.

As a result, DAPT trusts may not always serve as an effective asset protection and estate planning tool for real estate professionals residing in non-DAPT states, as creditors may collapse the trust structure.

Another significant development to consider is the Corporate Transparency Act (CTA), scheduled to become effective on January 1, 2024. This act will bring substantial changes to corporate reporting requirements in the United States.

It will require millions of companies and trusts to disclose information about their beneficial owners, individuals who hold ultimate ownership or control over the entity. This increased transparency may have implications for privacy, particularly for entities like LLCs, trusts, and corporations.

In summary, while DAPT asset protection structures offer valuable benefits to residents of DAPT states and non-U.S. residents, they may not provide the same level of protection for out-of-state residents.

For those seeking comprehensive asset protection solutions, offshore options, such as trusts in the Cook Islands, can be highly effective.

Swiss Bank Accounts for U.S. Residents

We assist U.S. residents with opening bank accounts in Switzerland and Liechtenstein in compliance with IRS regulations and FBAR reporting requirements.

What makes a Cook Islands Trust so attractive?

As the Cook Islands Trust became more ubiquitous and increasingly popular with American businesses, they have maintained a great reputation for security.

Any individual or business looking for powerful asset protection benefits, particularly those who are worried about future litigation, will want to consider this option.

A creditor who wishes to extract assets from a Cook Islands trust must re-try the case in the island nation where it was formed, in a jurisdiction known for its unfriendliness to creditors.

Even if the plaintiff chooses to go down this road, and many will not have the resources, they must provide proof “beyond a reasonable doubt”, not just the “preponderance of evidence” used in the United States.

In addition, the plaintiffs are required to pay legal fees and court costs upfront. It is also likely that the loser of the case will pay their own legal fees as well as the winner’s.

Additional Benefits:

Statute of limitations for a Cooks trust is one year.

Strength of asset protection statutes make the Cooks trust impenetrable, even by the federal government.

The laws surrounding Cook Islands trusts were written with Americans in mind and were actually written by a Colorado asset protection attorney.

The value of the assets is not disclosed, and it is against the law in the Cooks to identify who owns the trusts or to provide any information about them.

Cash and investment accounts, as well as real estate holdings, crypto and businesses, may be registered in the trusts, but unlike DAPTs none of these are required to be physically located in the Cooks.

Cook Islands, a self-governing state associated with New Zealand, offer a different type of secrecy: the long arm of United States law simply does not reach it. For example,

Federal Trade Commission (FTC) failed to collect a $37.5 million judgment against Kevin Trudeau, author of The Weight Loss Cure, for “airing blatantly deceptive infomercials.

Fannie Mae, a government-sponsored lender, was unable to collect on a $10 million judgment against Oklahoma real estate investor Andrew Grossman, despite a trial that dragged on for years.

Cook Islands Are Crypto-Friendly

Cook Islands Ministry of Finance and Economic Management (MFEM) recently modernized the trust industry by launching ‘Smart Trust platform’ built on a blockchain. This moved the traditional legal framework and processes onto a blockchain-based digital platform.

This program enables creation of Crypto Smart Asset Protection Trusts, which allows clients to manage their crypto assets and NFTs in a safe and trusted environment.

Crypto Smart Asset Protection Trusts built on the blockchain:

ensures privacy;

allows management and trading of cryptocurrencies inside placed inside of a trust;

ensures transparency between desired individuals (e.g., trust beneficiaries) but not available to the world at large;

allows transfer of digital asset ownership to the trust from any third party;

allows transfer of asset’s ownership out of the trust.

The use of Crypto Smart Asset Protection Trusts allows asset protection planners and clients access protection without the inherent problems and risks of traditional trusts. Smart Trusts efficiently combined the benefits of the traditional trust with blockchain technology, transcending limitations that existed in the ownership, management and administration of both cryptocurrency and physical assets.

Structure

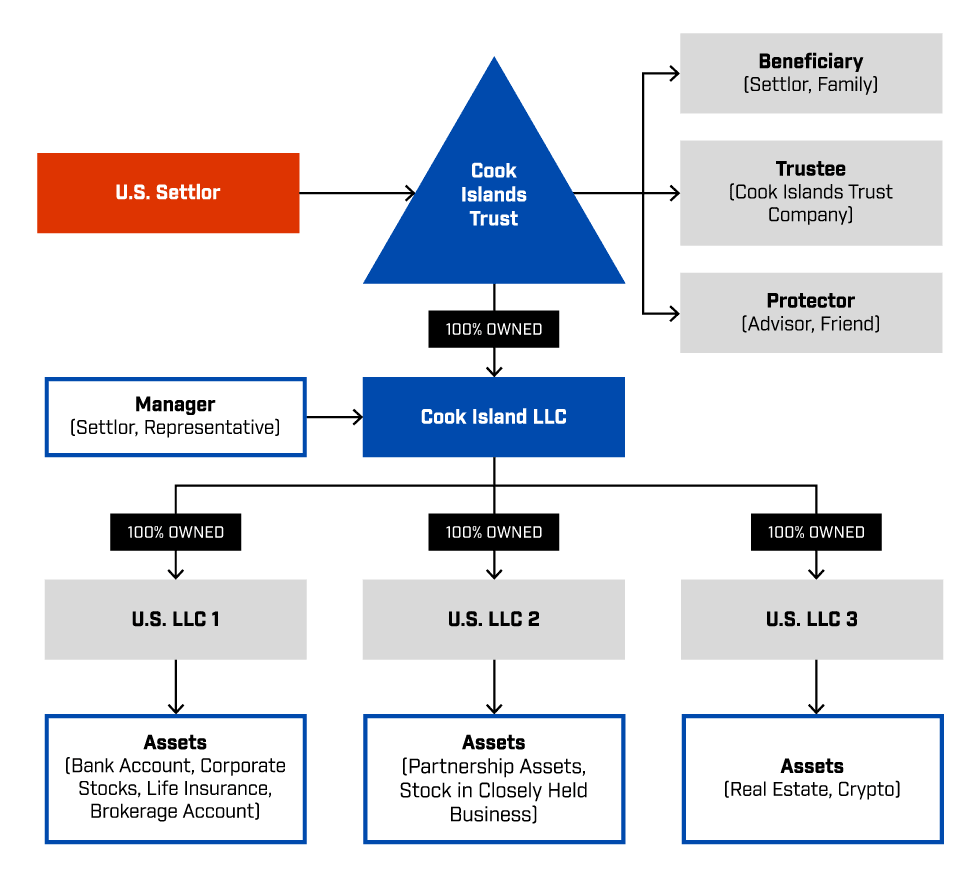

A typical Cook Islands Wealth Protection structure has several components allowing both flexibility and protection:

The Settlor establishes a Cook Islands International Trust

A Cook Islands licenced trustee serves as the Trustee

The flexible Trust structured allows the settlor and his family members to be appointed discretionary beneficiaries of the Trust

Protector can be appointed to monitor the activities of the Trustee, and can be granted absolute or veto powers or a combination of both

The Settlor can provide a letter to the Trustee detailing his/her wishes in regards to the investment and distribution of assets both during and after his/her lifetime

The Trust owns 100% of a limited liability company (“LLC”) incorporated in the Cook Islands, or other jurisdiction appropriate to the client’s circumstances

The Settlor, or his representative, is the Manager of the LLC

Assets are held and managed within the LLC or entities underlying it

Features

The Trustee is not required to be involved in the management of the LLC or its assets.

The Trustee can be granted power to remove and replace the Manager of the LLC incertain circumstances to protect the interests of the Manager and the assets under his/her control

The Manager is not personally liable for the debts, obligations or liabilities of the LLC

The Trustee is not subject to foreign judgements or forced heirship rules

Benefits

Assets held within the structure, including family businesses, can be managed and operated by the Settlor and his/her family without interference from the Trustee

The Settlor’s personal and business assets can be passed to the next generations in an orderly fashion in accordance with his/her wishes.

A change in Manager of the LLC does not give rise to fraudulent conveyance claims

Enhanced protection of assets from unforeseen creditors

Legitimate confidentiality of ultimate ownership of assets within the structure

What Assets Can Be Transferred into a Trust?

Bank and brokerage accounts

Shareholder stock from closely held corporations

Money market accounts, cash, checking and savings accounts

Cryptocurrrency, NFTs and other types of digital assets (Bitcoin, Ethereum, Stablecoins).

Partnership assets

Real estate

Life Insurance Policies

Vehicles: cars, boats, trucks, airplanes

Planning Considerations

Any offshore trust will have higher maintenance costs and setup fees, along with lengthier federal disclosures and IRS filings.

Despite being entirely ethical and legal, negative perceptions of impropriety often accompany offshore accounts. The settlor will also be required to relinquish control of the account to a foreign trustee.

As with any new trust plan, it is always wise to research the pros and cons before making any sudden moves.

The financial benefits of these trusts are numerous, including protection from lawsuits, strict confidentiality, no income taxes, no limits on the perpetuity of the trust, the flexibility to select managing trustees from one’s own country, zero impact from inheritance laws or court judgments from other countries.

Most people considering a Cook Islands trust will want to work with a trusted asset protection lawyer to determine if makes sense for their situation.

When a Cook Islands trust is selected for your asset protection plan, the legal team at Dilendorf Law Firm will provide the most strategic guidance.